JLARC staff created statewide database of county-level parcel data to analyze forest lands for the Legislature

JLARC staff compiled data from 32 counties

Each county uses its own data system to track parcel records, including whether each parcel is subject to the Forest Fire Protection Assessment (assessment). As a result, there is no centralized system for analyzing assessments.

JLARC staff created a statewide database with calendar year 2016 parcel and assessment records from 32 of the state's 39 counties:

- 5 counties do not have forest land subject to the assessment: Adams, Benton, Franklin, Grant, and Whitman.

- 2 counties, Lewis and Wahkiakum, did not respond to the JLARC request for data.

The database includes 2.8 million parcel records. The records have information such as parcels not subject to the assessment, taxable value, and fire district. The database created by JLARC staff contains more detailed information than the Department of Natural Resources (DNR) needs, to manage the program going forward. While DNR has some information about assessed parcels, it is outdated and potentially inaccurate. Sections 3 and 4 of this report address the steps needed to update DNR's assessment information. Appendix 1 describes the methodology in detail.

Nearly 5,500 parcels pay property tax as forest but do not pay the assessment

JLARC staff identified 5,455 parcels that are classified as forest for property tax purposes, but the owners do not pay the assessment.

- Land use codes indicate the parcels are noncommercial forest timberland, non-agricultural open space, or designated forestland under RCW 84.33.

- Some likely should be subject to the assessment. Considering current assessment rates and parcel size, JLARC staff estimate that the parcels could generate up to $179,000 in annual assessment fees.

- This list is not exhaustive: There are likely parcels with other land use codes that also should be subject to the assessment.

As noted in Section 3, JLARC staff also identified parcels that are cleared of trees but still subject to the assessment.

Without clear and consistent definitions and a comprehensive review of parcels, DNR cannot confirm whether it is appropriately collecting assessment fees across the state.

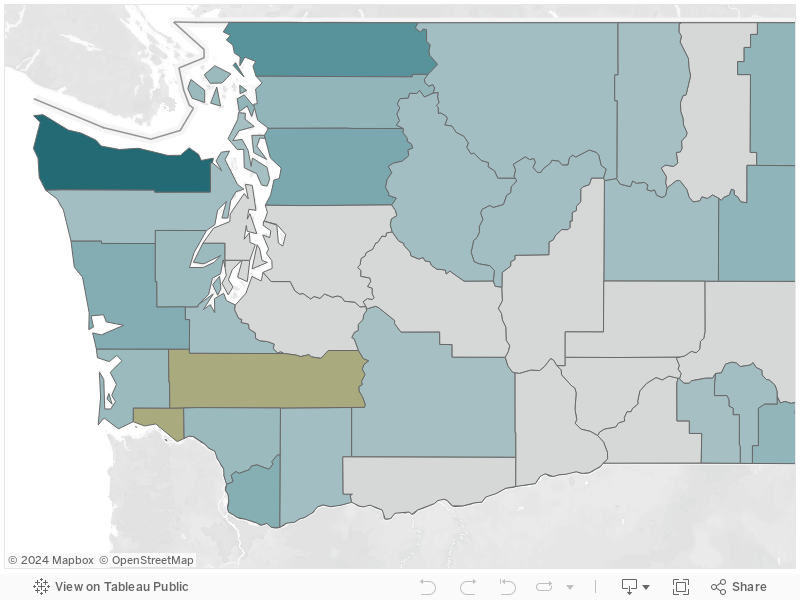

Exhibit 5.1: There are 5,455 parcels taxed as forest that do not pay the assessment

Source: County assessor parcel records for calendar year 2016. Calculations do not include: land categories that are excluded from the assessment; state owned lands; land owned by a tribe or held in trust for a tribe; federally owned land; tidal or shore lands.

More than 20,000 parcels exist where owners do not pay the assessment or a local fire district levy, but likely still protected by DNR or a district

JLARC staff found 20,135 parcels that do not pay the assessment or a local fire levy.

It is unclear whether the parcels should be subject to the assessment, a local fire district levy, or both. For example, from the data we received from assessors,

- 25 percent have some taxable improvements, which can include homes, outbuildings, fences, or other permanent construction.

- 14 percent have a state or local tax exemption. The county may not collect the assessment from tax-exempt owners, although the parcel is subject to the fee. DNR could bill these landowners directly.

The landowners likely would still receive fire suppression services. Title 52 RCW allows fire districts to recover costs of fire suppression on parcels that do not pay for fire protection. Statute also allows DNR to recover expenses incurred suppressing fires due to negligence. If assessed, these parcels would pay approximately $446,223.

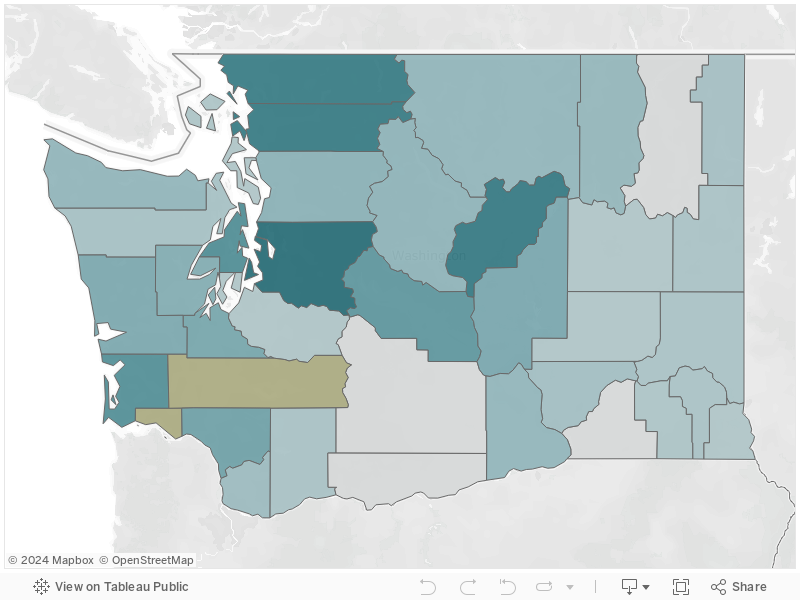

Exhibit 5.2: There are 20,135 parcels where owners do not pay for fire protection through the assessment or local levy

Source: JLARC staff analysis of calendar year 2016 parcel data from county assessors and DNR. JLARC staff analyzed all parcels in the state and excluded: parcels subject to the assessment, parcels that pay a local fire protection district levy, parcels owned by the federal government or Indian tribes, and parcels that are exempt from the assessment by DNR policy, such as swampland, and gravel pits.