|

JLARC Final Report: 2017 Tax Preference Performance Reviews |

Report 17-07, December 2017

Alternative Fuel Vehicles | Sales and Use Tax

Click here for One Page Overview

- Summary of this Review

- Details on this Preference

- Recommendations and Agency Response

- How We Do Reviews

- More about this Review

| The Preference Provides | Tax Type | Estimated Biennial Beneficiary Savings |

|---|---|---|

A sales and use tax exemption on the first $32,000 of a sale or lease agreement for qualifying new clean alternative fuel vehicles with a manufacturer's suggested retail price of $42,500 or less for the lowest price base model. The preference is scheduled to expire when one of the following occurs:

|

Sales and Use |

$14.8 million |

| Public Policy Objective |

|---|

The Legislature stated it wanted to increase the use of qualifying clean alternative fuel vehicles by reducing the price of such vehicles. |

| Recommendations |

|---|

|

Legislative Auditor’s Recommendation Review: The Legislature should review the preference in the 2019 legislative session if the number of qualifying vehicles titled in Washington has not reached 7,500. Commissioner Recommendation: The Commission endorses the Legislative Auditor’s recommendation with comment. The Legislature should review this preference and revisit its expectations for the number of qualifying vehicles. |

- 1. What is the preference?

- 2. Legal History

- 3. Other Relevant Background

- 4. Public Policy Objectives

- 5. Are Objectives Being Met?

- 6. Beneficiaries

- 7. Revenue and Economic Impacts

- 8. Other States with Similar Preference?

- 9. Applicable Statutes

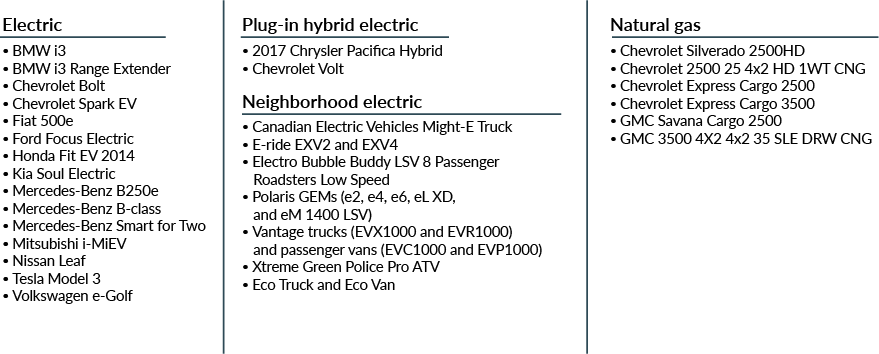

Sales and use tax exemption for purchases or leases of new vehicles that use clean alternative fuel

Purpose

The Legislature passed this sales and use tax preference with the stated purpose to increase the use of clean alternative fuel vehicles in Washington.

Clean alternative fuel vehicles are powered by electricity, natural gas, propane, or hydrogen and must meet specific emission standards.

Exemption applies to the first $32,000 of a sale for vehicles with base model priced at $42,500 or less

Individuals are exempt from paying sales or use tax on the first $32,000 of a sale or lease agreement for vehicles with a manufacturer’s suggested retail price of $42,500 or less for the lowest base model.

Qualifying vehicles must be either exclusively powered by a clean alternative fuel or plug-in hybrids that use electricity as at least one power source, and can travel at least 30 miles using only battery power.

The sales and use tax exemption has three components: the 6.5 percent state sales tax, an additional 0.3 percent sales tax for motor vehicle sales, and the applicable local sales tax.

Legislature set two potential expiration dates for the sales and use tax preference

The preference expires as soon as one of the following occurs:

- The cumulative number of qualifying vehicles titled in Washington on or after July 15, 2015, reaches 7,500.

- July 1, 2019.

Legislature has modified sales and use tax preference over time to encourage more use of clean alternative fuel vehicles

The first sales and use tax preference, passed in 2005, took effect January 1, 2009, when the first alternative fuel vehicles (AFVs) were expected to be on the market.

Since then, the Legislature has continued to modify the preference to encourage more use of qualifying AFVs.

2005: Legislature passed sales and use tax exemptions for new, clean AFVs and hybrids effective in 2009

The Legislature passed two sales and use tax exemptions for sales and leases of qualifying new passenger cars, light duty trucks, and medium duty passenger vehicles. Qualifying vehicles had to be powered by a clean alternative fuel or by hybrid technology with highway mileage ratings of at least 40 miles per gallon. There were no price limitations for qualifying vehicles.

The preferences were scheduled to expire January 1, 2011.

2009: Legislature repealed preference for new hybrid vehicles after 8 months, but left the preference for AFVs in place

The Legislature repealed the sales and use tax exemption for new hybrid technology vehicles with highway mileage ratings of at least 40 miles per gallon.

The Legislature did not change the preference for sales and leases of new vehicles powered only by clean alternative fuel.

2010: Legislature extended and expanded tax preference to include some used, modified AFVs

The Legislature expanded the preference to apply to qualifying used vehicles that were part of a fleet of five or more vehicles all owned by the same person. The used vehicles had to be modified after their initial purchase to run exclusively on a clean alternative fuel and meet other qualifying criteria.

The Legislature also extended the expiration date from January 1, 2011, to July 1, 2015.

2015: Legislature allowed preference to expire, then replaced with a modified version

After the existing tax preference expired on July 1, 2015, the Legislature passed a new, modified preference that took effect July 15, 2015.

The new exemption applied to sales and leases for the following vehicles with a sales or lease price of $35,000 or less:

- “Plug-in hybrid vehicles” - vehicles that use at least one power source that can be recharged by an external electricity source and can travel at least 30 miles using only battery power.

- Qualifying alternative fuel vehicles which are powered exclusively by natural gas, propane, hydrogen, or electricity.

The exemption no longer applied to sales or leases of used, modified vehicles.

The Legislature established a July 1, 2019, expiration date.

2016: Legislature revised current preference to include higher priced vehicles but lowered amount eligible for exemption

Effective July 1, the preference applies to the first $32,000 of a vehicle’s sales price or lease agreement on new qualifying vehicles with a manufacturer’s suggested retail price of $42,500 or less for the lowest base model.

The preference expires as soon as one of the following occurs:

- The total number of qualifying vehicles titled in Washington on or after July 15, 2015, reaches 7,500.

- July 1, 2019.

Other tax credits, exemptions, and Governor’s goals focus on increasing use of alternative fuel vehicles and clean fuel

The sales and use tax exemption is one of many tools used to encourage the use of alternative fuel vehicles and clean fuel.

Federal income tax credit up to $7,500 for plug-in electric vehicles

A federal income tax credit is currently available to people who purchase new, qualifying plug-in electric vehicles (PEVs). For vehicles purchased after December 31, 2009, the minimum credit is $2,500 and the maximum is $7,500. The credit amount is determined by the vehicle’s battery capacity and gross weight. The credit will phase out when a manufacturer’s cumulative sales reach 200,000 vehicles.

Governor’s Results Washington program established other clean transportation goals in 2011

Governor Inslee’s “Results Washington” program set a goal to increase the number of PEVs registered in Washington to 50,000 by 2020. This includes all PEVs, not just those that are exempt from sales and use tax.

Washington has passed other tax preferences for clean alternative vehicles, fuels, and infrastructure

In addition to the sales and use tax preference, the Legislature has passed several other preferences related to clean alternative fuel vehicles and related infrastructure.

| Preference | Description |

|---|---|

| Clean Alternative Fuel Commercial Vehicle B&O or Public Utility Tax (PUT) Credit | Credits for businesses purchasing or leasing a clean alternative fuel commercial vehicle or modifying a vehicle to use clean fuel. |

| EV Battery and Charging Station Sales and Use Tax Exemption Click here for 2017 JLARC review. | Exemption for purchases of batteries, component parts of EV infrastructure, and labor and services to install and repair batteries or infrastructure. |

| EV Leasehold Excise Tax (LET) Exemption Click here for 2017 JLARC review. | Exemption for private leases of public land to construct, install, or operate EV infrastructure. |

| EV Supply Equipment (EVSE) Return on Utility Investment Incentive | Utilities and Transportation Commission may approve an additional 2% to the standard return rate if the utility installs EVSE on a fully regulated basis like other capital investments. |

| Biodiesel Feedstock Sales and Use Tax Exemption | Exemptions for purchases of waste vegetable oil (cooking oil) from restaurants or commercial food processors that is used to produce biodiesel for personal use. |

| Alternative Fuel and Hybrid Electric Vehicle (HEV) Emissions Inspection Exemption | Exemption from state emissions control inspections on dedicated electric, natural gas, and propane vehicles, and HEVs with an EPA fuel economy rating of at least 50 MPG (city driving). |

| Natural Gas Used in Transportation - Various Preferences | Five preferences for the manufacturers and sellers of natural gas used for transportation. |

Legislature stated public policy objective in its performance statement

The Legislature stated it wanted to increase the use of qualifying clean alternative fuel vehicles by reducing the price of such vehicles.

Stated objective: Increase use of clean alternative fuel vehicle by reducing the price

The Legislature categorized the sales and use tax preference as intending to induce certain behaviors. The stated public policy objective was to:

“. . . . increase the use of clean alternative fuel vehicles in Washington . . . by extend[ing] the existing sales and use tax exemption on certain clean alternative fuel vehicles in order to reduce the price charged to customers for clean alternative fuel vehicles.”

Legislature provided metric for JLARC review

In 2016, the Legislature directed JLARC to report on the number of clean alternative fuel vehicles titled in the state to measure the effectiveness of the tax preference.

Legislature set two potential targets for when preference should end

The Legislature identified two targets for when the sales and use tax preference should expire. The preference will end when the first of these is reached:

- 7,500 qualifying new vehicles are titled in Washington on or after July 15, 2015.

- July 1, 2019.

Preference has reduced prices for qualifying vehicles but it is unknown the extent it is impacting sales

The preference has reduced the purchase and lease price of qualifying new clean alternative fuel vehicles (AFVs). Prices are reduced by the applicable sales tax rate for the first $32,000 of the sale or lease agreement.

| Price without preference | Price with preference | Savings with Preference | |

|---|---|---|---|

| Vehicle purchase price from dealer | $42,500 |

$42,500 |

|

| Cap on exemption | ($32,000) |

||

| Taxable amount | $42,500 |

$10,500 |

|

| Sales tax owed (Average rate – 9.3%) | $3,953 |

$977 |

|

| Total price paid | $46,453 |

$43,477 |

$2,976 |

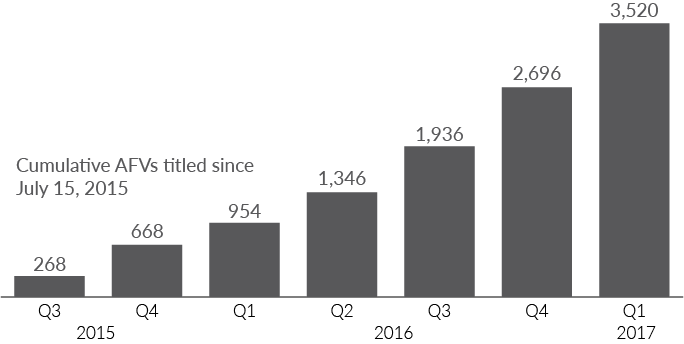

New AFV titles about halfway to 7,500 target

The Department of Licensing has issued 3,520 titles for qualifying vehicles since July 15, 2015. This represents 47 percent progress toward the 7,500 target. To reach 7,500 titles before the final expiration date of July 1, 2019, an additional 3,980 qualifying AFVs must be titled between April 1, 2017, and July 1, 2019. This equates to 442 per quarter.

Since July 1, 2016, the number of new titles per quarter has exceeded 442 and has increased each successive quarter. If this trend continues, the 7,500 target will be met before the final expiration date.

Throughout this period, the federal income tax credit for purchases of new, qualifying plug-in electric vehicles (PEVs) has remained in place.

New clean AFV titles less than 1% of all new titled vehicles in Washington

Department of Licensing data indicates that clean AFVs accounted for just 0.5 percent of new titles for vehicles of the same class in Fiscal Year 2016.

During the first five months of Fiscal Year 2017 (July through November 2016, the latest data available when this report was published), the share of AFVs increased to 0.9 percent of new vehicle titles for similar classes of vehicles.

Majority of new qualifying AFV titles are in Puget Sound region

Sixty percent of the newly titled qualifying alternative fuel vehicles were in King County between July 2015 and November 2016. Snohomish County and Pierce County were the second and third top counties for total number of new AFV titles.

Many other factors impact vehicle purchases

Continuing the tax preference beyond the expiration date will provide a reduction in the sale or lease price of qualifying vehicles for up to $32,000. While this may encourage people to purchase qualifying vehicles, other issues also influence vehicle purchasing decisions. These include:

- Purchase price of electric vehicles tend to be higher than conventional vehicles.

- High battery costs and concerns about battery range for electric vehicles.

- Average driving costs are lower for electric vehicles than gas-powered vehicles—The U.S. Department of Energy reports that it costs about one-half as much on average to drive an electric vehicle using electricity the same distance as a similar vehicle fueled by gasoline. The estimate uses national averages for gasoline and electricity prices.

- Access to charging stations.

- Washington and nine other states charge additional registration fees on AFVs.

Preference benefits buyers, lessees, and sellers of clean alternative fuel vehicles

Tax preferences have direct beneficiaries (entities whose state tax liabilities are directly affected) and may have indirect beneficiaries (entities that may receive benefits from the preference, but are not the primary recipient of the benefit).

Direct Beneficiaries

The direct beneficiaries are individuals, businesses, and public or private entities that purchase or lease a qualifying clean alternative fuel vehicle (AFV) in Washington.

The purchaser or lessee does not pay sales or use tax on up to $32,000 of the qualifying vehicle’s sale or lease agreement. Qualifying vehicles include:

- Vehicles powered exclusively by natural gas, propane, hydrogen, or electricity.

- Plug-in hybrids powered partly by an external electricity source that can travel at least 30 miles using only battery power.

Between July 15, 2015, and March 31, 2017, there have been 3,520 titles issued to individuals and other entities that have benefited from the preference.

Indirect Beneficiaries

Indirect beneficiaries are automobile dealers who sell or lease qualifying vehicles. The tax preference reduces the price of vehicles, especially when paired with available federal tax credits and other manufacturer or dealer offers.

Estimated beneficiary savings in 2017-19 Biennium are $14.8 million

JLARC staff estimate direct beneficiary savings of $3.9 million in Fiscal Year 2016 and $14.8 million for the 2017-19 Biennium.

The preference is currently scheduled to expire when the first of these occur: 7,500 qualifying vehicles are titled in Washington, since July 15, 2015, or July 1, 2019.

JLARC staff estimated the beneficiary savings using Department of Licensing data on qualifying new titles. It is unclear if the savings will increase or continue at the pace they did for the first nine months of Fiscal Year 2017.

If they do continue at the same pace, the total number of new titles could reach the 7,500 target to end the preference by the middle of Fiscal Year 2019.

| Biennium | Fiscal Year | Qualifying Vehicle Sales | State Sales Tax (includes 0.3% vehicles sales tax) | Local Sales Tax | Beneficiary Savings |

|---|---|---|---|---|---|

| 2015-17 7/1/15-6/30/17 | 2016 | $41,412,000 |

$2,816,000 |

$1,088,000 |

$3,904,000 |

| 2017 | $78,879,000 |

$5,364,000 |

$2,039,000 |

$7,403,000 |

|

| 2017-19 7/1/17-6/30/19 | 2018 | $78,879,000 |

$5,364,000 |

$2,039,000 |

$7,403,000 |

| 2019 | $78,879,000 |

$5,364,000 |

$2,039,000 |

$7,403,000 |

|

| 2017-19 Biennium | $157,758,000 |

$10,728,000 |

$4,078,000 |

$14,806,000 |

|

Without the tax preference, beneficiaries would pay sales or use tax, but impact on AFV use is uncertain

If the tax preference was allowed to expire, purchasers of qualifying AFVs and plug-in hybrids would pay sales or use tax on the full cost of the vehicle.

The impact of the preference on sales of qualifying vehicles is unknown. Many other issues influence whether consumers decide to purchase these vehicles.

States offer varying types of incentives to encourage use of clean alternative fuels and vehicles

Most states and the District of Columbia provide incentives to encourage use of alternative fuels and vehicles. The U.S. Department of Energy maintains an Alternative Fuel Data Center, tracking incentive programs offered in each state.

Only Washington and New Jersey provide sales and use tax exemptions for new purchases and leases of clean alternative fuel vehicles (AFVs).

States use a variety of other tools to encourage AFV adoption, including: income tax credits, rebates, grants, low interest loans, HOV lane access, free parking, reduced or exempted vehicle registrations, and emissions test exemptions.

RCW 82.08.809

Exemptions—Vehicles using clean alternative fuels and electric vehicles, exceptions—Quarterly transfers. (Contingent expiration date.)

(1)(a) Except as provided in subsection (4) of this section, the tax levied by RCW 82.08.020 does not apply to sales of new passenger cars, light duty trucks, and medium duty passenger vehicles, which (i) are exclusively powered by a clean alternative fuel or (ii) use at least one method of propulsion that is capable of being reenergized by an external source of electricity and are capable of traveling at least thirty miles using only battery power.

(b) Beginning with sales made or lease agreements signed on or after July 1, 2016, the exemption in this section is only applicable for up to thirty-two thousand dollars of a vehicle's selling price or the total lease payments made plus the selling price of the leased vehicle if the original lessee purchases the leased vehicle before the expiration of the exemption as described in subsection (6) of this section.

(2) The seller must keep records necessary for the department to verify eligibility under this section.

(3) As used in this section, "clean alternative fuel" means natural gas, propane, hydrogen, or electricity, when used as a fuel in a motor vehicle that meets the California motor vehicle emission standards in Title 13 of the California code of regulations, effective January 1, 2005, and the rules of the Washington state department of ecology.

(4)(a) A sale, other than a lease, of a vehicle identified in subsection (1)(a) of this section made on or after July 15, 2015, and before July 1, 2016, is not exempt from sales tax as described under subsection (1) of this section if the selling price of the vehicle plus trade-in property of like kind exceeds thirty-five thousand dollars.

(b) A sale, other than a lease, of a vehicle identified in subsection (1)(a) of this section made on or after July 1, 2016, and before the expiration of the exemption as described in subsection (6) of this section, is not exempt from sales tax as described under subsection (1)(b) of this section if, at the time of sale, the lowest manufacturer's suggested retail price, as determined in rule by the department of licensing pursuant to chapter 34.05 RCW, for the base model is more than forty-two thousand five hundred dollars.

(c) For leased vehicles for which the lease agreement was signed before July 1, 2015, lease payments are exempt from sales tax as described under subsection (1)(a) of this section regardless of the vehicle's fair market value at the inception of the lease.

(d) For leased vehicles identified in subsection (1)(a) of this section for which the lease agreement is signed on or after July 15, 2015, and before July 1, 2016, lease payments are not exempt from sales tax if the fair market value of the vehicle being leased exceeds thirty-five thousand dollars at the inception of the lease. For the purposes of this subsection (4), "fair market value" has the same meaning as "value of the article used" in RCW 82.12.010.

(e) For leased vehicles identified in subsection (1)(a) of this section for which the lease agreement is signed on or after July 1, 2016, and before the expiration of the exemption as described in subsection (6) of this section, lease payments are not exempt from sales tax as described under subsection (1)(b) of this section if, at the inception of the lease, the lowest manufacturer's suggested retail price, as determined in rule by the department of licensing pursuant to chapter 34.05 RCW, for the base model is more than forty-two thousand five hundred dollars.

(f) The department of licensing must maintain and publish a list of all vehicle models qualifying for the sales tax exemption under this section until the expiration of the exemption as described in subsection (6) of this section.

(5) On the last day of January, April, July, and October of each year, the state treasurer, based upon information provided by the department, must transfer from the multimodal transportation account to the general fund a sum equal to the dollar amount that would otherwise have been deposited into the general fund during the prior calendar quarter but for the exemption provided in this section. Information provided by the department to the state treasurer must be based on the best available data, except that the department may provide estimates of taxes exempted under this section until such time as retailers are able to report such exempted amounts on their tax returns. For purposes of this section, the first transfer for the calendar quarter after July 15, 2015, must be calculated assuming only those revenues that should have been deposited into the general fund beginning July 1, 2015.

(6)(a) The exemption under this section expires, effective with sales of vehicles delivered to the buyer or leased vehicles for which the lease agreement was signed, after the last day of the calendar month immediately following the month the department receives notice from the department of licensing under subsection (7)(b) of this section. All leased vehicles that qualified for the exemption before the expiration of the exemption must continue to receive the exemption as described under subsection (1)(b) of this section on lease payments due through the remainder of the lease.

(b) Upon receiving notice from the department of licensing under subsection (7)(b) of this section, the department must provide notice as soon as is practicable on its web site of the expiration date of the exemption under this section.

(c) For purposes of this subsection, even if the department of licensing provides the department with notice under subsection (7)(b) of this section before the end of the fifth working day of the month notice is required, the notice is deemed to have been received by the department at the end of the fifth working day of the month notice is required.

(d) If, by the end of the fifth working day of May 2019, the department has not received notice from the department of licensing under subsection (7)(b) of this section, the exemption under this section expires effective with sales of vehicles delivered to the buyer or leased vehicles for which the lease agreement was signed after June 30, 2019.

(e) Nothing in this subsection (6) may be construed to affect the validity of any exemption properly allowed by a seller under this section before the expiration of the exemption as described in (a) of this subsection and reported to the department on returns filed after the expiration of the exemption.

(f) Nothing in this subsection (6) may be construed to allow an exemption under this section for the purchase of a qualifying vehicle by the original lessee of the vehicle after the expiration of the exemption as provided in (a) of this subsection.

(7)(a) By the end of the fifth working day of each month, until the expiration of the exemption as described in subsection (6) of this section, the department of licensing must determine the cumulative number of qualifying vehicles titled on or after July 15, 2015, and provide notice of the cumulative number of these vehicles to the department.

(b) The department of licensing must notify the department once the cumulative number of qualifying vehicles titled in the state on or after July 15, 2015, equals or exceeds seven thousand five hundred.

(8) By the last day of July 2016, and every six months thereafter until the expiration of the exemption as described in subsection (6) of this section, based on the best available data, the department must report the following information to the transportation committees of the legislature: The cumulative number of qualifying vehicles titled in the state on or after July 15, 2015, as reported to it by the department of licensing; and the dollar amount of all state retail sales and use taxes exempted on or after July 15, 2015, under this section and RCW 82.12.809.

(9) For purposes of this section, "qualifying vehicle" means a vehicle qualifying for the exemption under this section or RCW 82.12.809 in which the sale was made or the lease agreement was signed on or after July 15, 2015.

[ 2016 1st sp.s. c 32 § 2; 2015 3rd sp.s. c 44 § 408; 2010 1st sp.s. c 11 § 2; 2005 c 296 § 1.]

NOTES:

Effective date—2016 1st sp.s. c 32: "This act takes effect July 1, 2016." [ 2016 1st sp.s. c 32 § 4201

Tax preference performance statement—2016 1st sp.s. c 32: "This section is the tax preference performance statement for the tax preferences contained in sections 2 and 3 of this act. The performance statement is only intended to be used for subsequent evaluation of the tax preference. It is not intended to create a private right of action by any party or be used to determine eligibility for preferential tax treatment.

(1) The legislature categorizes the tax preference as one intended to induce certain designated behavior by taxpayers, as indicated in RCW 82.32.808(2)(a).

(2) It is the legislature's specific public policy objective to increase the use of clean alternative fuel vehicles in Washington. It is the legislature's intent to extend the existing sales and use tax exemption on certain clean alternative fuel vehicles in order to reduce the price charged to customers for clean alternative fuel vehicles.

(3) To measure the effectiveness of the tax preferences in sections 2 and 3 of this act in achieving the public policy objectives described in subsection (2) of this section, the joint legislative audit and review committee must evaluate the number of clean alternative fuel vehicles titled in the state.

(4) In order to obtain the data necessary to perform the review in subsection (3) of this section, the department of licensing must provide data needed for the joint legislative audit and review committee analysis. In addition to the data source described under this subsection, the joint legislative audit and review committee may use any other data it deems necessary." [ 2016 1st sp.s. c 32 § 1.]

Tax preference performance statement—2015 3rd sp.s. c 44 §§ 408 and 409: "This section is the tax preference performance statement for the tax preferences contained in sections 408 and 409 of this act. The performance statement is only intended to be used for subsequent evaluation of the tax preference. It is not intended to create a private right of action by any party or be used to determine eligibility for preferential tax treatment.

(1) The legislature categorizes the tax preference as one intended to induce certain designated behavior by taxpayers, as indicated in RCW 82.32.808(2)(a).

(2) It is the legislature's specific public policy objective to increase the use of clean alternative fuel vehicles in Washington. It is the legislature's intent to extend the existing sales and use tax exemption on certain clean alternative fuel vehicles in order to reduce the price charged to customers for clean alternative fuel vehicles.

(3) To measure the effectiveness of the tax preferences in sections 408 and 409 of this act in achieving the public policy objectives described in subsection (2) of this section, the joint legislative audit and review committee must evaluate the number of clean alternative fuel vehicles registered in the state.

(4) In order to obtain the data necessary to perform the review in subsection (3) of this section, the department of licensing must provide data needed for the joint legislative audit and review committee analysis. In addition to the data source described under this subsection, the joint legislative audit and review committee may use any other data it deems necessary." [ 2015 3rd sp.s. c 44 § 407.]

Effective date—2005 c 296: "This act takes effect January 1, 2009." [ 2005 c 296 § 5200

RCW 82.12.809

Exemptions—Vehicles using clean alternative fuels and electric vehicles, exceptions—Quarterly transfers.

(1)(a) Except as provided in subsection (4) of this section, the provisions of this chapter do not apply in respect to the use of new passenger cars, light duty trucks, and medium duty passenger vehicles, which (i) are exclusively powered by a clean alternative fuel or (ii) use at least one method of propulsion that is capable of being reenergized by an external source of electricity and are capable of traveling at least thirty miles using only battery power.

(b) Beginning with purchases made or lease agreements signed on or after July 1, 2016, the exemption in this section is only applicable for up to thirty-two thousand dollars of a vehicle's purchase price or the total lease payments made plus the purchase price of the leased vehicle if the original lessee purchases the leased vehicle before the expiration of the exemption as described in RCW 82.08.809(6).

(2) The definitions in RCW 82.08.809 apply to this section.

(3) A taxpayer is not liable for the tax imposed in RCW 82.12.020 on the use, on or after the expiration of the exemption as described in RCW 82.08.809(6), of a passenger car, light duty truck, or medium duty passenger vehicle that is exclusively powered by a clean alternative fuel or uses at least one method of propulsion that is capable of being reenergized by an external source of electricity and is capable of traveling at least thirty miles using only battery power, if the taxpayer used such vehicle in this state before the expiration of the exemption as described in RCW 82.08.809(6), and the use was exempt under this section from the tax imposed in RCW 82.12.020.

(4)(a) For vehicles identified in subsection (1)(a) of this section purchased on or after July 1, 2016, and before the expiration of the exemption as described in RCW 82.08.809(6), or for leased vehicles identified in subsection (1)(a) of this section for which the lease agreement was signed on or after July 1, 2016, and before the expiration of the exemption as described in RCW 82.08.809(6), a vehicle is not exempt from use tax as described under subsection (1)(b) of this section if, at the time the tax is imposed for purchased vehicles or at the inception of the lease for leased vehicles, the lowest manufacturer's suggested retail price, as determined in rule by the department of licensing pursuant to chapter 34.05 RCW, for the base model is more than forty-two thousand five hundred dollars.

(b) For vehicles identified in subsection (1)(a) of this section purchased on or after July 15, 2015, and before July 1, 2016, or for leased vehicles identified in subsection (1)(a) of this section for which the lease agreement was signed on or after July 15, 2015, and before July 1, 2016, a vehicle is not exempt from use tax if the fair market value of the vehicle exceeds thirty-five thousand dollars at the time the tax is imposed for purchased vehicles, or at the inception of the lease for leased vehicles.

(c) For leased vehicles for which the lease agreement was signed before July 1, 2015, lease payments are exempt from use tax as described under subsection (1)(a) of this section regardless of the vehicle's fair market value at the inception of the lease.

(5) On the last day of January, April, July, and October of each year, the state treasurer, based upon information provided by the department, must transfer from the multimodal transportation account to the general fund a sum equal to the dollar amount that would otherwise have been deposited into the general fund during the prior calendar quarter but for the exemption provided in this section. Information provided by the department to the state treasurer must be based on the best available data. For purposes of this section, the first transfer for the calendar quarter after July 15, 2015, must be calculated assuming only those revenues that should have been deposited into the general fund beginning July 1, 2015.

(6)(a) The exemption provided under this section does not apply to the use of new passenger cars, light duty trucks, and medium duty passenger vehicles, or lease payments due on such vehicles, if the date of sale of the vehicle from the seller to the buyer occurred or the lease agreement was signed after the expiration of the exemption as provided in RCW 82.08.809(6).

(b) All leased vehicles that qualified for the exemption before the expiration of the exemption must continue to receive the exemption as described under subsection (1)(b) of this section on lease payments due through the remainder of the lease.

(c) Nothing in this subsection (6) may be construed to allow an exemption under this section for the purchase of a qualifying vehicle by the original lessee of the vehicle after the expiration of the exemption.

[ 2016 sp.s. c 32 § 3; 2015 3rd sp.s. c 44 § 409; 2010 1st sp.s. c 11 § 3; 2005 c 296 § 3.]

NOTES:

Effective date—Tax preference performance statement—2016 sp.s. c 32: See notes following RCW 82.08.809.

Effective date—2015 3rd sp.s. c 44: See note following RCW 46.68.395.

Tax preference performance statement—2015 3rd sp.s. c 44 §§ 408 and 409: See note following RCW 82.08.809.

Effective date—2005 c 296: See note following RCW 82.08.809.

- Legislative Auditor Recommendation

- Letter from Commission Chair

- Commissioners' Recommendation

- Agency Response

Legislative Auditor recommends reviewing the tax preference before the final expiration date if the target for vehicle titles is not yet met

The Legislature should review the sales and use tax preference for clean alternative fuel vehicles in the 2019 legislative session if the number of qualifying vehicles titled in Washington has not reached 7,500.

The preference reduces the price of the sale or lease agreement for qualifying new alternative fuel vehicles. However, it is unknown the extent the preference is impacting sales. Other factors also influence vehicle purchasing decisions.

As of March 31, 2017, 3,520 qualifying vehicles were titled, which is 47 percent of the 7,500 target. If this trend continues, the target will be met before the final expiration date. If that target is not met, the preference will expire on July 1, 2019.

Legislation required: To be determined (preference expires July 1, 2019).

Fiscal impact: Depends on legislative action.

The Commission endorses the Legislative Auditor’s recommendation with comment.

The Legislature should review this preference and revisit its expectations for the number of qualifying vehicles.