|

JLARC Final Report: 2017 Tax Preference Performance Reviews |

Report 17-07, December 2017

Coal-Fired Power Plant Preferences | Multiple Taxes

Click here for One Page Overview

- Summary of this Review

- Details on this Preference

- Recommendations and Agency Response

- How We Do Reviews

- More about this Review

| The Preference Provides | Tax Type | Estimated Biennial Beneficiary Savings |

|---|---|---|

A sales and use tax exemption for purchases of coal used in electric generation. |

Sales and Use Tax |

$6.1-16.6 million in the 2017-19 biennium |

A sales and use tax exemption for purchases of air pollution control equipment. |

Sales and Use Tax |

$0 in the 2017-19 biennium |

A property tax exemption for the assessed value of air pollution control equipment. |

Property Tax |

$2.2 million in the 2017-19 biennium |

| Public Policy Objective |

|---|

The Legislature's stated public policy objectives:

|

| Recommendations |

|---|

Legislative Auditor’s Recommendation Continue: The Legislature should continue the three tax preferences until the coal-fired boilers at the plant are decommissioned. The three tax preferences are meeting the stated public policy objectives of helping Washington’s only coal-fired power plant to update air pollution control equipment, abate pollution, and play an economic role in its community through 2025. Commissioner Recommendation: The Commission endorses the Legislative Auditor’s recommendation without comment. |

- 1. What are the Preferences?

- 2. Legal History

- 3. Other Relevant Background

- 4. Public Policy Objectives

- 5. Are Objectives Being Met?

- 6. Beneficiaries

- 7. Revenue and Economic Impacts

- 8. Other States with Similar Preference?

- 9. Applicable Statutes

Three tax preferences for coal-fired electric power plants

Purpose

The Legislature passed three preferences with the stated purpose to help certain thermal electric generation facilities (power plants) to:

- Update air pollution control equipment/facilities.

- Abate pollution.

- Play a long-term economic role in their communities.

Statute defines eligibility

A thermal electric generation facility is a power plant that converts heat energy (e.g., from burning coal) into electricity.

Plants that started operating between December 1969 and July 1975 are eligible for the tax preferences. JLARC staff identified only one eligible plant currently operating in Washington: a coal-fired electric power plant in Centralia.

Three preferences: two for sales and use tax, one for property tax

The Legislature passed a bill in 1997 that enacted these three preferences. They do not have expiration dates.

| Preference | Description | Effective Date | Expiration Date |

|---|---|---|---|

| Coal

Purchases (Sales & Use Tax) |

Exempts sales and use of coal at eligible power plants. | January 1, 1999 | None |

| Air

pollution control equipment (Sales & Use Tax) |

Exempts sales and use of personal property, labor, and services related to the installation of air pollution control equipment/facilities. | May 15, 1997 | None |

| Air

pollution control equipment (Property Tax) |

Exempts air pollution control equipment/facilities constructed or installed after May 15, 1997. | May 15, 1997 | None |

More detail on each preference can be found in the Other Relevant Background section.

The preferences arose from efforts to reduce air pollution

1995-1997: Coal-fired power plant ordered to limit sulfur dioxide emissions

The federal government amended the Federal Clean Air Act in 1990 and required power plants to control emissions such as sulfur dioxide.

In 1995, the Southwest Washington Air Pollution Control Authority ordered the coal-fired Centralia power plant to cut its sulfur dioxide emissions in half by 2001. Two years later, a second order required a 90 percent cut by 2003, limiting emissions to 10,000 tons per year. The cost of installing the necessary equipment/facilities was estimated to be $200 million.

1997: Legislature enacted three preferences for coal power plants

The Legislature created three tax preferences for coal power plants:

- A sales and use tax exemption for coal purchases.

- A sales and use tax exemption for sales of personal property, labor, or services for air pollution control equipment/facilities installation.

- A property tax exemption for air pollution control equipment/facilities installation.

The exemption for coal purchases required that at least 70 percent of the coal be local. That is, the coal had to be produced in either the county where the plant was located or a neighboring county. The Legislature repealed this requirement in 2000.

The three preferences have no expiration dates.

2007 – 2017: Legislature made additional changes to reduce greenhouse gas emissions from coal-fired power plants

In 2007, the Legislature created greenhouse gas emission performance standards. In 2009, Governor Gregoire issued an executive order requiring the Department of Ecology and the Centralia plant to develop a plan to comply with the standards by December 31, 2025.

In 2011, the Legislature amended the law to give the Centralia plant until 2025 to comply with the emission performance standards. The bill also required the plant to:

- Install additional pollution control technology.

- Make a total of $55 million in financial assistance payments to the community. The payments would end if the sales tax exemptions were repealed.

TransAlta, which owns the plant, announced it would transition away from coal and indicated it may convert to natural gas. The 2017 Legislature passed a sales and use tax exemption for converting a coal-fired power plant into a natural gas-fired plant or a biomass energy facility. This exemption was vetoed by the governor.

Definitions and more preference detail found in statute

Air pollution control equipment and facilities are defined in statute

Statute uses the terms “air pollution control equipment” and “air pollution control facilities.” Both are defined as:

“any treatment works, control devices and disposal systems, machinery, equipment, structures, property, property improvements, and accessories, that are installed or acquired for the primary purpose of reducing, controlling, or disposing of industrial waste that, if released to the outdoor atmosphere, could cause air pollution, or that are required to meet regulatory requirements applicable to their construction, installation, or operation.”

Sulfur dioxide scrubbers are one type of air pollution control equipment/facility at the Centralia plant. These scrubbers spray a wet limestone slurry onto the exhaust from burning coal to capture sulfur dioxide.

Centralia also uses selective non-catalytic reduction, which reduces emissions of nitrogen oxides. This technology uses a chemical reaction to convert nitrogen oxides into less harmful gases and water vapor.

More about eligibility

Plants that started operating between December 1969 and July 1975 are eligible for the tax preferences.

Sales and use tax exemption on coal purchases

This preference exempts purchases of coal from retail sales and use taxes. To be eligible for the exemption, the owners of the power plant must:

- Apply to the Department of Revenue (DOR) for the exemption;

- Demonstrate to the Department of Ecology that they have made initial and continued progress to install air pollution control equipment/facilities to meet applicable regulatory requirements established under state or federal law, including the Washington Clean Air Act; and

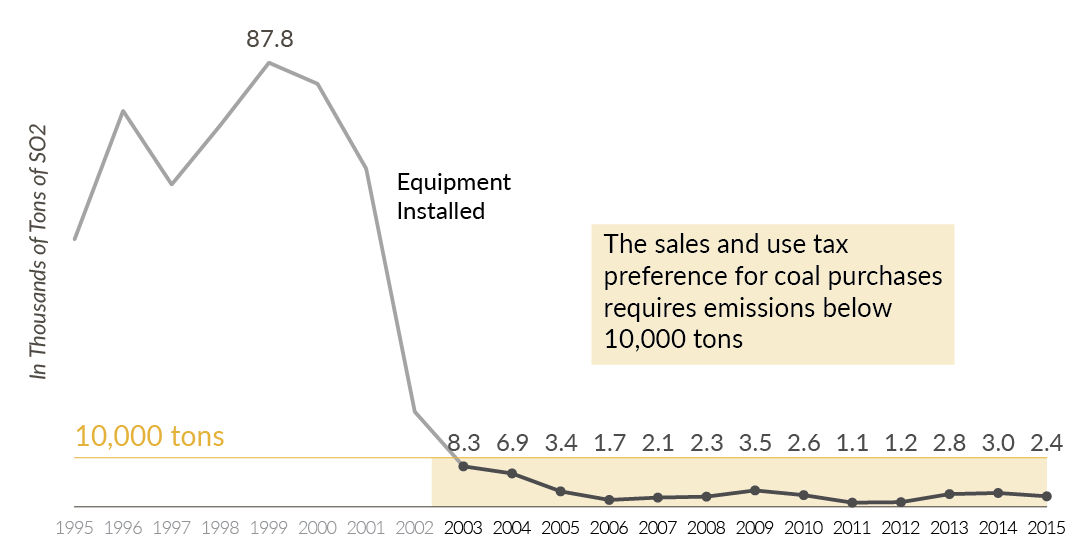

- Emit no more than 10 thousand tons of sulfur dioxide during the previous 12 months.

If a regional air pollution control authority or the Department of Ecology finds the plant’s sulfur dioxide emissions exceed the limit, the plant will lose the tax exemption. It may reapply for the exemption when it meets the emission requirements.

Sales and use tax exemption for air pollution control equipment/facilities

This preference exempts the following from sales and use tax:

- Sales of tangible personal property to a light and power business for construction or installation of air pollution control equipment/facilities at a coal power plant; or

- Labor and services performed for construction or installation of air pollution control equipment/facilities.

To qualify for the preference, the equipment/facilities must be constructed or installed after May 15, 1997 and meet state or federal regulatory requirements. The preference excludes maintenance or repairs of pollution control equipment/facilities.

The preference includes a claw-back provision. If electricity production at the plant falls below 20 percent annual capacity between 2003 and 2023, the plant must pay back a portion of previously exempted tax.

Property tax exemption for air pollution control equipment/facilities

This preference exempts air pollution control equipment/facilities constructed or installed after May 15, 1997, from property taxation. Owners must maintain records to identify annual beginning and ending asset balance of the pollution control equipment/facilities and explain the depreciation method used.

The Legislature stated three public policy objectives in its intent statement

The Legislature stated its intent to help coal power plants to:

- Update their air pollution control equipment/facilities.

- Abate pollution.

- Play a long-term economic role in the communities where they are located.

The public policy objectives are being met

The Centralia plant has updated its air pollution control equipment/facilities

Since the preferences were enacted, the Centralia plant, which is the only existing coal-fired power plant in Washington, has completed two installations of air pollution control equipment/facilities.

| Equipment/Facilities | Pollution Removed | Year Installed |

|---|---|---|

| Sulfur dioxide scrubbers | Sulfur dioxide | 2001- 02 |

| Selective non-catalytic reduction | Nitrogen oxide | 2011-12 |

The Centralia plant has reduced sulfur dioxide emissions

The sales and use tax preference for coal is contingent on the plant emitting less than 10 thousand tons of sulfur dioxide in any 12-month period. Sulfur dioxide emissions from the Centralia plant fell from a peak of 87.8 thousand tons in 1999 and have been below 10 thousand tons since 2003.

The Centralia plant continues to play an economic role in its community

The Centralia plant’s economic contribution includes employment and direct financial assistance:

- The plant has consistently employed more than 200 employees since 2001.

- TransAlta, which owns the Centralia plant, has made annual financial assistance payments of $4.58 million to support the community and energy development, as required by the 2011 agreement. From 2012 through 2016, these payments have totaled $22.9 million. According to the agreement, the payments will total $55 million by 2023: $10 million for weatherization, $20 million for economic and community development, and $25 million for developing energy technology.

The TransAlta coal-fired power plant in Centralia is the sole beneficiary of the preferences

Tax preferences have direct beneficiaries (entities whose state tax liabilities are directly affected) and indirect beneficiaries (entities that may receive benefits from the preference, but are not the primary recipient of the benefit).

Direct beneficiaries

The sponsor of the bill creating the preferences identified the Centralia plant as the beneficiary in committee testimony. Today, this plant is owned by TransAlta.

The plant notes its net generating capacity is 1,340 megawatts, and that its fuel (coal) is delivered by train from the Powder River Basin in Montana and Wyoming. Ranking behind two hydroelectric generating facilities, the Centralia plant has the third-largest generating capacity in Washington.

Indirect beneficiaries

Indirect beneficiaries may include:

- Sellers of coal and the air pollution control equipment/facilities.

- Residents and businesses in Centralia, Lewis County, and South Thurston County, to the extent that they benefit from the financial assistance payments.

Beneficiary savings vary by preference. Beneficiary savings will decline as the Centralia plant transitions away from coal.

Each of the three preferences has different revenue and economic impacts.

Beneficiary savings from the coal exemption depend on the price and amount of coal

JLARC staff based its beneficiary savings estimate on Energy Information Administration (EIA) data showing the price and the amount of coal used for electric generation in Washington. EIA lists only one coal-fired electric power plant: TransAlta’s Centralia plant. The estimate for local sales taxes is based on the rate in unincorporated Lewis County.

The estimated range is based on two estimates of the taxable value of coal sales. The lower estimate uses only the commodity cost of the coal, while the higher estimate includes the cost of transporting the coal from the Powder River Basin in Wyoming and Montana to Centralia.

| Biennium | Fiscal Year | Estimated State Sales/Use Tax |

Estimated Local Sales Sales/Use Tax |

Estimated Total Beneficiary Savings |

|---|---|---|---|---|

| 2013-15 7/1/13-6/30/15 |

2014 | $3.9-$10.6 million |

$80-$210 thousand |

$3.9-$10.8 million |

| 2015 | $2.9-$8.1 million |

$60-$160 thousand |

$3.0-$8.3 million |

|

| 2015-17 7/1/15-6/30/17 |

2016 | $3.0-$8.1 million |

$60-$160 thousand |

$3.0-$8.3 million |

| 2017 | $3.0-$8.1 million |

$60-$160 thousand |

$3.0-$8.3 million |

|

| 2017-19 7/1/17-6/30/19 |

2018 | $3.0-$8.1 million |

$60-$160 thousand |

$3.0-$8.3 million |

| 2109 | $3.0-$8.1 million |

$60-$160 thousand |

$3.0-$8.3 million |

|

| 2017-19 Biennium |

$5.9-$16.3 million |

$120-$320 thousand |

$6.1-$16.6 million |

Sales and use tax exemption for air pollution control equipment/facilities was last used for equipment/facilities installed in in 2011-12

TransAlta noted that, based on the statute requiring compliance with the emission performance standard by 2025, it does not currently plan to have qualifying expenditures in the forecast period, so JLARC staff estimates no beneficiary savings for this preference.

According to TransAlta, the last two installations of air pollution control equipment/facilities that qualified for the tax preference were:

- Installation of sulfur dioxide scrubbers in 2001-2002, at a cost of $200 million.

- Installation of technology to reduce nitrogen oxide in 2011-2012, at a cost of $17 million.

Based on sales and use tax rates in effect at the time, JLARC staff estimate these expenditures would have resulted in beneficiary savings of $13.2 million and $1.1 million, respectively.

Property tax exemption beneficiary savings average $1.1 million per year

The Department of Revenue reviewed this preference in its 2016 tax exemption study and calculated the following savings.

| Biennium | Fiscal Year | Estimated State Property Tax Savings |

Estimated Local Property Tax Savings |

Estimated Total Property Tax Savings |

|---|---|---|---|---|

| 2015-17 7/1/15-6/30/17 |

2016 | $214,000 |

$961,000 |

$1,175,000 |

| 2017 | $189,000 |

$875,000 |

$1,064,000 |

|

| 2017-19 7/1/17-6/30/19 |

2018 | $194,000 |

$910,000 |

$1,104,000 |

| 2109 | $199,000 |

$946,000 |

$1,145,000 |

|

| 2017-19 Biennium |

$393,000 |

$1,856,000 |

$2,249,000 |

Total beneficiary savings from all three preferences are expected to decline as the plant ends coal-fired generation

- As the Centralia plant transitions from burning coal by 2025, coal purchases and beneficiary savings attributable to those purchases will reduce to zero.

- TransAlta noted that it does not currently plan to have qualifying expenditures for air pollution control equipment/facilities in the forecast period, so JLARC staff estimates no future beneficiary savings for this preference.

- As the assessed value of existing air pollution control equipment/facilities depreciates, property tax savings are expected to decline.

Absent the tax preferences, the beneficiary would pay the taxes, but not the financial assistance payments

Terminating the tax preferences would:

- Impose sales and use taxes on coal purchases.

- Impose sales and use taxes on the installation of additional air pollution control equipment/facilities.

- Impose property taxes on the assessed value of air pollution control equipment/facilities.

Any increased sales tax revenue from a repeal would be partially offset by the loss of the remaining annual $4.58 million financial assistance payments. The statute governing the Centralia plant’s transition away from coal-fired generation specifies that if the sales tax exemptions for coal or pollution control equipment/facilities are repealed, the balance of the $55 million in financial assistance payments are no longer required.

JLARC staff identified other states that provide tax relief for coal sales

Other states generate at least some of their power from coal-fired power plants, and some exempt coal from sales tax.

Because the sales and use tax preference for coal has the largest fiscal impact of the three preferences, the JLARC staff review of other states focused on the tax treatment of coal purchases. The review centered on the tax provisions governing coal in the ten states that use the most coal to generate electricity. All burn significantly more coal than Washington. Of these ten states:

- Illinois and Indiana impose sales tax for purchases of coal used to generate electricity.

- Pennsylvania exempts all retail sales and uses of coal.

- Texas, Ohio, Kentucky, and West Virginia have specific sales tax exemptions for the purchase of coal or fuel used to generate electricity.

- Missouri, Michigan, and Wyoming exempt coal consumed in manufacturing under more general manufacturing or industrial processing exemptions.

| 2015 Rank | State | Tons | Tax Treatment of Coal |

|---|---|---|---|

| 1 | Texas | 86,779

|

Fuel for thermal electric generation exempt |

| 2 | Illinois | 43,446

|

Taxable |

| 3 | Indiana | 38,734

|

Taxable |

| 4 | Missouri | 38,468

|

Coal consumed in manufacturing of any product exempt |

| 5 | Kentucky | 34,380

|

Coal sales for electric generation exempt |

| 6 | Pennsylvania | 31,391

|

All retail coal sales exempt |

| 7 | Ohio | 30,518

|

Coal sales for electric generation exempt |

| 8 | Michigan | 29,487

|

Fuel consumed for an industrial processing activity (including electric generation) exempt |

| 9 | West Virginia | 28,223

|

Coal sales for electric generation exempt |

| 10 | Wyoming | 26,313

|

Fuel used in manufacturing or processing exempt |

| … | … | … | … |

| 34 | Washington | 3,405

|

Coal for thermal electric generation exempt |

Findings—Intent—1997 c 368 (reviser’s note to RCW 82.08.810):

"(1) The legislature finds that:

(a) Thermal electric generation facilities play an important role in providing jobs for residents of the communities where such plants are located; and

(b) Taxes paid by thermal electric generation facilities help to support schools and local and state government operations.

(2) It is the intent of the legislature to assist thermal electric generation facilities placed in operation after December 31, 1969, and before July 1, 1975, to update their air pollution control equipment and abate pollution by extending certain tax exemptions and credits so that such plants may continue to play a long-term vital economic role in the communities where they are located." [ 1997 c 368 § 1.]

RCW 82.08.811

Exemptions—Coal used at coal-fired thermal electric generation facility—Application—Demonstration of progress in air pollution control—Notice of emissions violations—Reapplication—Payments on cessation of operation.

(1) For the purposes of this section:

(a) "Air pollution control facilities" means any treatment works, control devices and disposal systems, machinery, equipment, structure, property, property improvements, and accessories, that are installed or acquired for the primary purpose of reducing, controlling, or disposing of industrial waste that, if released to the outdoor atmosphere, could cause air pollution, or that are required to meet regulatory requirements applicable to their construction, installation, or operation; and

(b) "Generation facility" means a coal-fired thermal electric generation facility placed in operation after December 3, 1969, and before July 1, 1975.

(2) Beginning January 1, 1999, the tax levied by RCW 82.08.020 does not apply to sales of coal used to generate electric power at a generation facility operated by a business if the following conditions are met:

(a) The owners must make an application to the department of revenue for a tax exemption;

(b) The owners must make a demonstration to the department of ecology that the owners have made reasonable initial progress to install air pollution control facilities to meet applicable regulatory requirements established under state or federal law, including the Washington clean air act, chapter 70.94 RCW;

(c) Continued progress must be made on the development of air pollution control facilities to meet the requirements of the permit; and

(d) The generation facility must emit no more than ten thousand tons of sulfur dioxide during a previous consecutive twelve-month period.

(3) During a consecutive twelve-month period, if the generation facility is found to be in violation of excessive sulfur dioxide emissions from a regional air pollution control authority or the department of ecology, the department of ecology shall notify the department of revenue and the owners of the generation facility shall lose their tax exemption under this section. The owners of a generation facility may reapply for the tax exemption when they have once again met the conditions of subsection (2)(d) of this section.

(4) *RCW 82.32.393 applies to this section.

[ 1997 c 368 § 4.]

RCW 82.08.810

Exemptions—Air pollution control facilities at a thermal electric generation facility—Exceptions—Exemption certificate—Payments on cessation of operation.

(1) For the purposes of this section, "air pollution control facilities" mean any treatment works, control devices and disposal systems, machinery, equipment, structures, property, property improvements, and accessories, that are installed or acquired for the primary purpose of reducing, controlling, or disposing of industrial waste that, if released to the outdoor atmosphere, could cause air pollution, or that are required to meet regulatory requirements applicable to their construction, installation, or operation.

(2) The tax levied by RCW 82.08.020 does not apply to:

(a) Sales of tangible personal property to a light and power business, as defined in RCW 82.16.010, for construction or installation of air pollution control facilities at a thermal electric generation facility; or

(b) Sales of, cost of, or charges made for labor and services performed in respect to the construction or installation of air pollution control facilities.

(3) The exemption provided under this section applies only to sales, costs, or charges:

(a) Incurred for air pollution control facilities constructed or installed after May 15, 1997, and used in a thermal electric generation facility placed in operation after December 31, 1969, and before July 1, 1975;

(b) If the air pollution control facilities are constructed or installed to meet applicable regulatory requirements established under state or federal law, including the Washington clean air act, chapter 70.94 RCW; and

(c) For which the purchaser provides the seller with an exemption certificate, signed by the purchaser or purchaser's agent, that includes a description of items or services for which payment is made, the amount of the payment, and such additional information as the department reasonably may require.

(4) This section does not apply to sales of tangible personal property purchased or to sales of, costs of, or charges made for labor and services used for maintenance or repairs of pollution control equipment.

(5) If production of electricity at a thermal electric generation facility for any calendar year after 2002 and before 2023 falls below a twenty percent annual capacity factor for the generation facility, all or a portion of the tax previously exempted under this section in respect to construction or installation of air pollution control facilities at the generation facility shall be due as follows:

| Year event occurs | Portion of previously exempted tax due |

2003

|

100%

|

2004

|

95%

|

2005

|

90%

|

2006

|

85%

|

2007

|

80%

|

2008

|

75%

|

2009

|

70%

|

2010

|

65%

|

2011

|

60%

|

2012

|

55%

|

2013

|

50%

|

2014

|

45%

|

2015

|

40%

|

2016

|

35%

|

2017

|

30%

|

2018

|

25%

|

2019

|

20%

|

2020

|

15%

|

2021

|

10%

|

2022

|

5%

|

2023

|

0%

|

(6) *RCW 82.32.393 applies to this section.

[ 1997 c 368 § 2.]

RCW 82.12.811

Exemptions—Coal used at coal-fired thermal electric generation facility—Application—Demonstration of progress in air pollution control—Notice of emissions violations—Reapplication—Payments on cessation of operation.

(1) For the purposes of this section:

(a) "Air pollution control facilities" means any treatment works, control devices and disposal systems, machinery, equipment, structure, property, property improvements, and accessories, that are installed or acquired for the primary purpose of reducing, controlling, or disposing of industrial waste that, if released to the outdoor atmosphere, could cause air pollution, or that are required to meet regulatory requirements applicable to their construction, installation, or operation; and

(b) "Generation facility" means a coal-fired thermal electric generation facility placed in operation after December 3, 1969, and before July 1, 1975.

(2) Beginning January 1, 1999, the provisions of this chapter do not apply in respect to the use of coal to generate electric power at a generation facility operated by a business if the following conditions are met:

(a) The owners must make an application to the department of revenue for a tax exemption;

(b) The owners must make a demonstration to the department of ecology that the owners have made reasonable initial progress to install air pollution control facilities to meet applicable regulatory requirements established under state or federal law, including the Washington clean air act, chapter 70.94 RCW;

(c) Continued progress must be made on the development of air pollution control facilities to meet the requirements of the permit; and

(d) The generation facility must emit no more than ten thousand tons of sulfur dioxide during a previous consecutive twelve-month period.

(3) During a consecutive twelve-month period, if the generation facility is found to be in violation of excessive sulfur dioxide emissions from a regional air pollution control authority or the department of ecology, the department of ecology shall notify the department of revenue and the owners of the generation facility shall lose their tax exemption under this section. The owners of a generation facility may reapply for the tax exemption when they have once again met the conditions of subsection (2)(d) of this section.

(4) *RCW 82.32.393 applies to this section.

[ 1997 c 368 § 6.]

RCW 82.12.810

Exemptions—Air pollution control facilities at a thermal electric generation facility—Exceptions—Payments on cessation of operation.

(1) For the purposes of this section, "air pollution control facilities" mean any treatment works, control devices and disposal systems, machinery, equipment, structures, property, property improvements, and accessories, that are installed or acquired for the primary purpose of reducing, controlling, or disposing of industrial waste that, if released to the outdoor atmosphere, could cause air pollution, or that are required to meet regulatory requirements applicable to their construction, installation, or operation.

(2) The provisions of this chapter do not apply in respect to:

(a) The use of air pollution control facilities installed and used by a light and power business, as defined in RCW 82.16.010, in generating electric power; or

(b) The use of labor and services performed in respect to the installing of air pollution control facilities.

(3) The exemption provided under this section applies only to air pollution control facilities that are:

(a) Constructed or installed after May 15, 1997, and used in a thermal electric generation facility placed in operation after December 31, 1969, and before July 1, 1975; and

(b) Constructed or installed to meet applicable regulatory requirements established under state or federal law, including the Washington clean air act, chapter 70.94 RCW.

(4) This section does not apply to the use of tangible personal property for maintenance or repairs of the pollution control equipment or to labor and services performed in respect to such maintenance or repairs.

(5) If production of electricity at a thermal electric generation facility for any calendar year after 2002 and before 2023 falls below a twenty percent annual capacity factor for the generation facility, all or a portion of the tax previously exempted under this section in respect to construction or installation of air pollution control facilities at the generation facility shall be due according to the schedule provided in RCW 82.08.810(5).

(6) *RCW 82.32.393 applies to this section.

[ 2003 c 5 § 12;1997 c 368 § 3.]

RCW 84.36.487

Air pollution control equipment in thermal electric generation facilities—Records—Payments on cessation of operation.

(1) Air pollution control equipment constructed or installed after May 15, 1997, by businesses engaged in the generation of electric energy at thermal electric generation facilities first placed in operation after December 31, 1969, and before July 1, 1975, shall be exempt from property taxation. The owners shall maintain the records in such a manner that the annual beginning and ending asset balance of the pollution control facilities and depreciation method can be identified.

(2) For the purposes of this section, "air pollution control equipment" means any treatment works, control devices and disposal systems, machinery, equipment, structures, property, property improvements, and accessories, that are installed or acquired for the primary purpose of reducing, controlling, or disposing of industrial waste that, if released to the outdoor atmosphere, could cause air pollution, or that are required to meet regulatory requirements applicable to their construction, installation, or operation.

(3) *RCW 82.32.393 applies to this section.

[ 1997 c 368 § 11.]

- Legislative Auditor Recommendation

- Letter from Commission Chair

- Commissioners’ Recommendation

- Agency Response

Legislative Auditor recommends continuing the three preferences

The Legislature should continue the three tax preferences until the coal-fired boilers at the plant are decommissioned. The tax preferences are meeting the stated public policy objectives of helping Washington’s only coal-fired power plant to update air pollution control equipment/facilities, abate pollution, and play an economic role in its community through 2025.

As the Centralia plant transitions from burning coal by 2025, coal purchases and beneficiary savings attributable to those purchases will reduce to zero. Further, state statute and the memorandum of agreement between the owner, TransAlta, and the state provide that repeal of the tax preferences would mean any remaining financial assistance payments to the community are no longer required.

Legislation required: No (preferences have no expiration dates).

Fiscal impact: None.

The Commission endorses the Legislative Auditor’s recommendation without comment.