Analyzing Development Costs for Low-Income Housing

Legislative Auditor's Conclusion:

Development costs for six projects are consistent with independent

estimates. Commerce can improve cost controls, and the Housing Finance Commission has

opportunities to lower costs by examining for-profit developer involvement.

In 2017, the Legislature directed JLARC to analyze the costs of developing low-income

housing (i.e., affordable to households making less than 80 percent of the area median

income). JLARC staff reviewed the two largest programs in Washington.

Low-Income Housing Tax Credit (LIHTC)

Housing Trust Fund (HTF)

Managing agency

Washington State Housing Finance Commission (Commission)

Department of Commerce (Commerce)

Type of subsidy

Federal tax credits and tax-exempt bonds

State grants and low-interest loans

Multifamily housing financing awarded (2017)

$644 million in tax credits and $732 million in bonds

$54 million

Multifamily units financed (2017)*

7,049

1,785

* Some projects may have received both LIHTC and HTF funds and

units are included in both counts.

Source: Washington State Housing Finance Commission and Department of Commerce.

Six case studies found development costs were within or below estimates expected by

independent experts

JLARC worked with professional cost estimators who

calculated retrospective estimates for six LIHTC projects completed between 2014 and

2016. JLARC staff found that the costs were within or below the estimated cost ranges.

Commerce does not collect final development costs for Housing Trust Fund projects, so

it was not possible to conduct a similar analysis for that program.

Analysis shows location, developer type, and project characteristics affect costs.

Program restrictions and population needs can limit the ability to change some of

these factors.

Statistical analysis of 241 LIHTC projects showed that location, developer type, and

project characteristics are factors most likely to affect development costs. There was

insufficient information to determine how prevailing wage and environmental building

requirements affect costs.

The ability to alter some factors may be limited. For example, having more

bedrooms per unit may not be appropriate for housing that serves single adults.

Influencing the type of developer raises broader policy issues beyond development

costs. Stakeholders noted nonprofit and housing authority developers may be best

suited to serve more vulnerable populations once developments are operational. As a

result, those developers may fulfill more scoring criteria than for-profit

developers when competing for certain funding. Commission policy encourages

for-profit developers and nonprofit organizations to develop projects as co-owners.

This has not occurred.

The Commission follows key best practices for monitoring and controlling costs,

while Commerce can improve its cost controls

The Commission follows most best practices published by the National Council of State

Housing Agencies. Commerce does not collect final development costs, limiting its

ability to analyze and monitor cost data over time.

Legislative Auditor Recommendations

The Commission should identify and evaluate options for increasing the involvement

of for-profit developers in the 9% tax credit program and report their findings to

the Legislature.

Commerce should collect final development cost data from Housing Trust Fund

recipients to improve cost controls.

Commerce and the Commission should report development cost data to the Legislature

annually.

The Commission and Commerce concur with these recommendations. You can find

additional information on the Recommendations tab.

Committee Addendum

The Committee agrees with the recommendations of the Legislative Auditor, but wishes

to caution readers against drawing unsupported conclusions from the study.

We emphasize that the analysis of factors affecting development costs, with details

in Appendix B, establishes correlation, but not causation. This retrospective study

shows that, on average, for-profit developers are involved with less costly

developments. However, the analysis does not establish that this correlation is

caused by less costly projects attracting more for-profit developers; neither does it

establish that for-profit developers cause the projects to become less costly.

In the committee hearing on the preliminary report, we heard testimony that some

housing projects focus on serving the needs of specific populations by integrating

space for service providers or other amenities. Further analysis of these amenities

might clarify significant cost components and further illuminate differences between

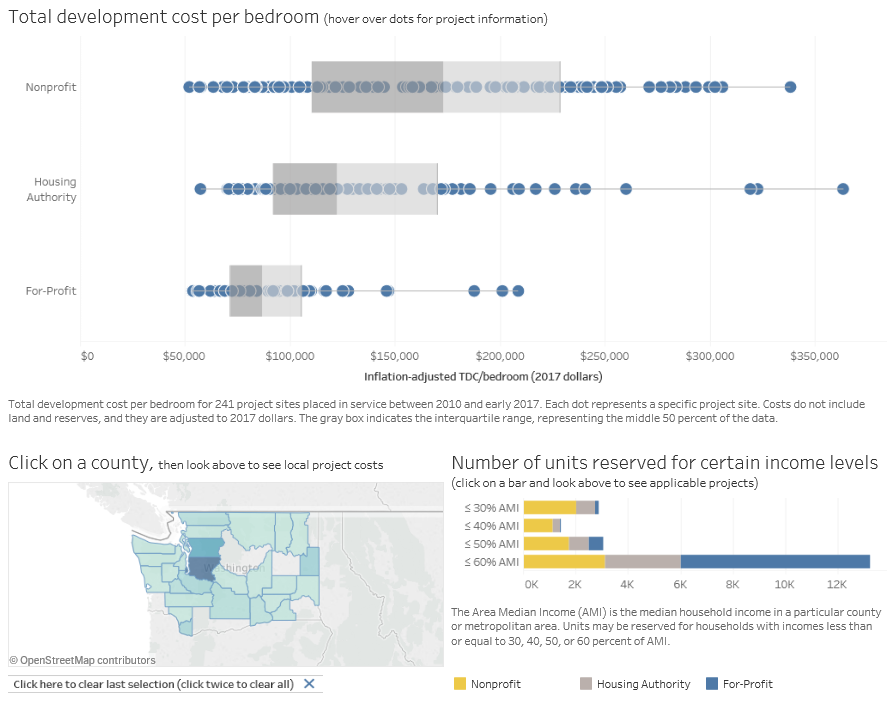

developer types. Additionally, as shown in Exhibit B1, most units built by for-profit

developers allow income levels up to 60% of Area Median Income (AMI), while units

restricted to 50%, 40%, or 30% AMI are almost entirely built by governmental or

non-profit developers. This again suggests that different developer types are serving

different populations, which may have a significant impact on costs.

Committee Action to Distribute Report

On January 10, 2019 this report was approved for distribution by the Joint

Legislative Audit and Review Committee.

Action to distribute this report does not imply the Committee agrees or disagrees

with Legislative Auditor recommendations.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

1. Two programs finance low-income housing

The Washington State Housing Finance Commission and the

Department of Commerce manage programs that finance low-income housing development

Two main programs offer incentives for the development of low-income housing

Two programs provide the majority of funding and have financed the most units in

Washington: the Low-Income Housing Tax Credit program and the Housing Trust Fund. Most

of this housing serves low-wage workers, farm workers, people experiencing

homelessness, persons with disabilities, seniors, and other populations.

Washington State Housing Finance Commission offers federal tax credits (LIHTC

program)

The Washington State Housing Finance Commission (Commission) administers the

Low-Income Housing Tax Credit program, commonly called LIHTC (pron.

"lie-tech"). The program finances construction of low-income housing through

federal tax incentives.

Housing financed by LIHTC must be affordable to households with incomes at 60 percent

or less than the area median (26 US Code § 42 (g)(1)(B)). Once built, housing must

remain affordable to low-income tenants for at least 30 years.

Developers use credits to secure funding from investors

The program provides an indirect subsidy to housing developers.

The Internal Revenue Service (IRS) provides federal tax credits for the

development of low-income housing. The tax credits are allocated at the state

level.

The Commission awards the state's tax credits to developers. Developers may

receive a 9% tax credit or a combination of a 4% tax credit and tax-exempt

bonds (see below).

A developer transfers the credits to an investor that funds the housing. The

investor becomes a majority owner of the housing, and uses the credit to reduce its

federal income tax liability.

The developer uses the money received from the investor to build low-income

housing.

Exhibit 1.1: LIHTC offers incentives in two ways: a 9% tax credit or tax-exempt

bonds plus a 4% credit

9% Tax Credit

Bond/4% Tax Credit

Description

Provides tax credits that typically generate equity for 70% of a project's

development costs.

Provides tax credits that typically generate equity for 30% of a project's

development costs as long as 50% of the costs are financed by tax-exempt bonds.

Commission award process

The IRS limits available tax credit. Demand typically exceeds the amount of

available tax credit.

Projects are financed through a competitive process with criteria set by

the Commission.

The IRS does not limit tax credit but does limit tax-exempt bonds. Demand has

not exceeded the amount of available bonds.

Projects are financed if they meet Commission program criteria.

Recipients

Nonprofits and housing authorities

For-profit developers are eligible but have not received the tax credit in

over five years.

Nonprofits, housing authorities, and for-profit developers.

Population served

Households with lower incomes or special needs (e.g., supportive housing for

the homeless).

Households with slightly higher incomes (e.g., workforce housing).

Units developed (2009-16)

7,026

14,177

Source: JLARC staff analysis.

Department of Commerce offers grants and loans through the Housing Trust Fund

The Department of Commerce (Commerce) administers the Housing Trust Fund, a state

program that makes grants and low-interest loans for low-income housing. The maximum

award is $3 million per project. The Housing Trust Fund serves households with 80

percent or below the area median income (RCW 43.185A.010). Once built, housing must

remain affordable for at least 40 years.

Commerce must use a competitive process and award funds to nonprofit or government

developers

Use a competitive application process that evaluates applicants against statutory

criteria.

Allocate funds to nonprofit or government developers (e.g., tribes, local

governments, housing authorities). For-profit developers are not eligible.

Give preference to applications based on criteria such as commitment to serve

populations with the greatest need, providing housing for people with the lowest

incomes, and leveraging other funding sources.

Although statutory direction to prioritize costs when evaluating applications expired

in 2013, Commerce continues to consider costs when awarding funds. The Legislature can

allocate Housing Trust Fund dollars to specific developments.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

2. Costs are within estimated ranges

Six case studies found development costs were within or below

estimates expected by independent experts

JLARC staff reviewed six completed Low-Income Housing Tax Credit (LIHTC) projects to

evaluate costs

The Legislature directed JLARC to compare the costs of developing subsidized

low-income and market-rate housing. Like other researchers and entities such as the

Government Accountability Office that have reviewed this question, JLARC was unable to

obtain comparable data from market-rate developers. In the absence of this data, JLARC

contracted with a team of independent cost estimating professionals to develop

retrospective estimates for six projects that received LIHTC funding. The

retrospective estimates enabled a comparison of expected costs with actual costs.

Each project was funded by the Low-Income Housing Tax Credit (LIHTC) program (either

the 9% tax credit or a combination bond/4% tax credit). These case studies reflect

various regions, developer types (e.g., nonprofit, for-profit), populations served,

and construction years. More detail about the sites used in the case studies is

available in Appendix

A.

Total development costs were within or below ranges calculated by professional cost

estimators

JLARC staff hired professional cost estimators to calculate a retrospective cost

estimate for each housing development. The estimators:

Reviewed architectural drawings.

Considered market conditions, wage requirements, and other federal, state, and

local requirements in place during development.

Considered construction conditions that affected cost or time (e.g., labor supply,

site contamination).

Considered the cost effect of the state's green building performance standard (the

Evergreen Sustainable Development StandardWashington's green building performance standard required of

all low-income housing projects financed through LIHTC or the Housing Trust

Fund.), required by RCW

39.35D.080.

Completed site visits and interviews with industry professionals.

The estimators provided a range of estimated total development costs for each case

study. The costs include materials, labor, architect fees, loan fees, and other costs.

JLARC staff compared the cost estimates to actual total development costs reported to

the LIHTC program. The actual costs are within or below the estimated ranges.

Exhibit 2.1: Case studies of six LIHTC projects found actual development costs are

within or below estimated ranges

Source: JLARC staff depiction of six LIHTC projects, the retrospective estimates of

costs, and actual costs.

LIHTC development costs are reviewed during and after development

The Commission requires the owner of the LIHTC-financed property to monitor costs

during development. In addition, lenders and investors often monitor costs to ensure

that funds are spent appropriately. Monitoring may include site visits and use of

third-party architects to ensure construction quality.

After a project is built, the Commission requires the developer to submit a final

cost certification prepared by an independent Certified Public Accountant.

Analysis of a small sample of Seattle sites indicates challenges in comparing

LIHTC developments with market-rate projects

With the assistance from the Department of Housing and Urban Development (HUD), JLARC

staff compared LIHTC and market-rate development costs for a sample of multifamily

projects that participated in a HUD-insured mortgage program. In a comparison of 13

market-rate and 11 LIHTC projects in Seattle, LIHTC projects cost 8 percent more per

unit than market-rate projects.

The comparison highlighted some differences between the market-rate and LIHTC housing

developments that may contribute to cost differences:

LIHTC projects include the developer's compensation in the development costs. In

contrast, market-rate developers are compensated through the rental or sale of the

development. By excluding the developer's profit in the development costs,

market-rate costs may appear lower than LIHTC costs.

The LIHTC developments had fewer units, but units typically had more bedrooms and

more square footage than the market-rate developments.

Outside of this sample, it is unknown how LIHTC development costs compare with

market-rate costs because comprehensive and verifiable market-rate data is unavailable

for a full comparison.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

3. Analysis identifies factors that affect development costs

Statistical analysis of all 241 LIHTC project sites from

2009-2016 shows location, developer type, and project characteristics affect costs. The

Housing Finance Commission has opportunities to lower cost by examining for-profit

involvement.

What is a regression analysis?

Regression analysis is a commonly accepted statistical tool that estimates

the relationship between a factor (explanatory variable) and an outcome

(dependent variable). The analysis holds other factors constant so the

researcher can evaluate one at a time.

Regression analysis helps identify which factor(s) have a high likelihood of

affecting costs. It also helps estimate the size of each factor's impact.

See Appendix B for more information about interpreting regression results.

JLARC staff used a regression analysis to assess factors that may affect

development costs. These costs include materials, labor, architect fees, and other

costs, but exclude land costs and reserves. The analysis included 241 sites built

between 2009 and 2016 with funding from the Low-Income Housing Tax Credit (LIHTC)

program (for project data, see Exhibit B1 in Appendix

B). JLARC staff used data from the Washington State Housing Finance Commission

(Commission) and the U.S. Census. This is the first complete analysis of Washington’s

LIHTC data and helps identify cost drivers and actions that may be available to

control costs.

Regression approach: Many factors may affect development costs. JLARC staff

modeled the relationship between development costs and factors such as construction

year, developer type, location, and size. The models analyzed cost per unit, cost per

square foot, and cost per bedroom. The cost per bedroom model had the greatest

explanatory power and was generally consistent with the other models, so it is

presented here. Additional information and results for the cost per unit and per

square foot models are in Appendix

B.

For-profit and vertically integrated developers are associated with lower costs

The regression analysis suggests for-profit developers and vertically integrated

developers are associated with lower costs (see Exhibit 3.2). For this analysis,

vertically integrated is defined as developers also serving as their own general

contractor or having a shared interest with the project's general contractor.

These findings are consistent with similar research. However, influencing the type of

developer raises broader policy issues beyond development costs.

For-profit companies developed 38 percent of the projects financed with the bond/4%

tax credit program from 2009-2016. However, Commission scoring criteria favor

nonprofit developer and housing authority participation in the 9% tax credit program

(see Exhibit 3.1). The 9% tax credit is intended for housing projects that serve the

lowest income populations or those with specific service needs. Nonprofits and housing

authorities with missions to serve these populations fulfill more scoring criteria

than for-profit developers. For-profit developers may be more competitive for the 9%

tax credit if they partner with a nonprofit or housing authority as co-owners. This

has not occurred. JLARC staff found that for-profit developers have not received the

9% tax credit since 2013.

Exhibit 3.1: 241 LIHTC projects placed in service from 2010-2017 by developer

type

Source: JLARC staff statistical analysis of LIHTC data.

According to the Government Accountability Office and Oregon’s housing finance

agency, for-profits have developed projects using the 9% tax credit in other

states.

Developers with a high level of development activity are more likely to be vertically

integrated. Stakeholders noted that nonprofits and housing authorities may not have

enough construction work to afford becoming vertically integrated.

Exhibit 3.2: Developer type associated with lower development costs

All else being equal, if a developer is:

Predicted development cost per bedroom is:

For example, a development that costs:

A nonprofit or a housing authority

15-28% more than if the developer were a for-profit.

Vertically integratedVertically

integrated developers also serve as their own general contractor or have a

shared interest with the project's general contractor.

11% less than if the developer were not vertically

integrated.

Source: JLARC staff statistical analysis of LIHTC and U.S. Census data.

Location and other project characteristics also impact costs, but the ability to

control these characteristics may be limited by the needs of the population served

The regression analysis suggests that location and new construction can increase

costs. Rehabilitation projects or building more units or bedrooms may reduce costs

(see Exhibit 3.3). See Appendix

B for more information about how development factors can affect costs.

Still, it may be difficult for the Commission or the Department of Commerce to change

these cost factors.

Location: Some of the people served live in King County or in neighborhoods

with higher rent, older housing stock, or higher poverty.

New construction versus rehabilitation: In some areas, new construction

projects may be the only option if sites suitable for rehabilitation are not

available.

Building size: Building more units or bedrooms may depend upon need,

population served, funding, acreage available, and zoning. For example, constructing

more bedrooms per unit may not be appropriate for a development serving single

adults in an urban setting. Likewise, constructing additional units may not be

appropriate for a development located in an area with a small population.

Exhibit 3.3: Location and project characteristics associated with changes to

development costs

All else being equal, if a development is:

Predicted development cost per bedroom is:

For example, a development that costs:

Located in Seattle/King County

More than a project in the Non-Metro region The Commission divides the state into three geographic

regions: Seattle/King County, Metro (Clark, Pierce, Snohomish, Spokane, and

Whatcom counties), and Non-Metro (all other counties). . (The

regression found no significant relationship when comparing costs for the Metro

region and the Non-Metro regions.)

Located in a neighborhood with higher rent

More than a project in an area with lower rent.

Located in a neighborhood with older housing stock

More than a project in an area with newer housing stock.

Located in a neighborhood with higher poverty rates

More than a project in an area with a lower poverty rate.

New construction

More than a rehabilitation project.

A project with more units

Less than a project with fewer units.

A project with more bedrooms per unit

Less than a project with fewer bedrooms per unit.

Source: JLARC staff statistical analysis of LIHTC and U.S. Census data.

Consultants and stakeholders identified other factors that may affect development

costs but were not possible to isolate in the analysis

Wage requirements: State, local, and federal laws require that prevailing

wages be paid for developments that receive certain state, local, or federal funds.

Developers suggested that wage requirements may increase development cost by

increasing labor rates or limiting the number of general contractors willing to bid on

the project. However, it was not possible to evaluate this statement with statistical

analysis due to a lack of reliable data. Further, a review of the wage requirements in

six case studies of LIHTC projects was inconclusive (see Appendix

A).

Legislation passed in 2018 may affect the future impact of wage requirements. SSB

5493, which took effect September 2018, changed how prevailing wage rates are

calculated. Staff at the Department of Labor and Industries thought the change might

increase the overall minimum prevailing wage rates for construction projects,

including low-income housing projects. Labor and Industries notes the level of

increase depends on many factors, such as specific trades involved in a project and

local collective bargaining agreements. JLARC staff analyzed a selection of wage rates

and found that average wage rates increase with the new method.

Environmental requirements: Projects funded by the LIHTC or the Housing Trust

Fund must comply with the state's Evergreen Sustainable

Development Standard (ESDS)Washington's green building

performance standard required of all low-income housing projects financed through

LIHTC or the Housing Trust Fund.. Since all projects in this study

must comply with the standard, JLARC staff had no comparison group for a statistical

analysis of the standard's impact on costs. For six case studies of LIHTC projects,

cost estimators believe that compliance with the standards increased costs by up to 4

percent (see Appendix

A).

Legislative Auditor Recommendation

The Commission should identify and evaluate options for increasing the involvement

of for-profit developers in the 9% tax credit program and report their findings to

the Legislature.

The Commission concurs with this recommendation. You can find additional information

on the Recommendations tab.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

4. Agencies can improve reporting and controlling costs

The Commission follows key best practices for monitoring and

controlling costs, while Commerce can improve its cost controls

JLARC staff assessed agency policies for monitoring and controlling costs for

projects funded through the Low-Income Housing Tax Credit (LIHTC) program and Housing

Trust Fund.

The Washington State Housing Finance Commission has procedures to ensure reasonable

development costs

JLARC staff compared the Commission's practices to best practices published by the

National Council of State Housing Agencies (NCSHA).

The Commission follows best practices for monitoring and controlling costs for

projects in the LIHTC program. For example, it ensures costs are reasonable by

setting limits and giving developers with lower costs an advantage for competitive

awards.

After a project is built, the Commission requires the developer to submit a final

cost certification prepared by an independent Certified Public Accountant.

Commerce collects some cost data but does not track final development cost

Commerce reviews total development cost estimates when developers apply for Housing

Trust Fund (HTF) money and monitors costs during construction. Since 2002, Commerce

has contracted with a third-party construction inspector, the Washington Community Reinvestment Association (WCRA)WCRA

is a nonprofit that provides financing to low-income housing

developers., to review expenses and conduct site inspections during

construction. Commerce does not track final development costs after a project is

completed. Without final development cost data, Commerce cannot analyze development

costs of projects funded with Housing Trust Fund money or compare actual expenses to

estimates in the project applications.

At the Legislature's direction, Commerce identified 14 actions in 2009 and 2012 to

increase the cost effectiveness of the HTF program. One of the actions is to monitor

final development costs. Because Commerce does not collect this data, it is unable to

implement its own recommendation to document and monitor development cost data over

time.

Legislative Auditor Recommendations

Commerce should collect final development cost data from Housing Trust Fund

recipients to improve cost controls.

Commerce and the Commission should report total development cost data to the

Legislature annually.

The Commission and Commerce concur with these recommendations. You can find

additional information on the Recommendations tab.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

5. Subsidized programs limit developers' options

While construction is similar to market-rate housing, low-income

housing program requirements limit flexibility in financing, operating incomes, and

ability to sell

While comparing development costs of subsidized low-income and market-rate housing

was not possible, JLARC staff compared life cycle processes for both types of housing.

There are four life cycle processes that developers of low-income or market-rate

housing must consider: financing, construction, operations, and sale. As directed by

the Legislature, this report focuses on development (financing and construction).

Financial differences at later stages may limit a developer's ability to generate

income through rental or sale of the property.

Exhibit 5.1: There are important differences in regulatory requirements for

developing and managing low-income and market-rate housing

Source: JLARC staff analysis.

Low-income financing is more complicated and time-consuming

Low-income housing programs require multiple funding sources. A single development

may receive a loan from a bank, an equity contribution from a private investor, and

public funding at the local, state, and federal levels.

This financing structure complicates low-income housing development:

Application, public participation, and distribution of funds from multiple sources

may slow the timing of site acquisition, permitting, and construction.

Each funding source may require separate applications, inspections, monitoring,

and legal services.

Each funding source may require compliance with additional federal, state, and

local policies and priorities. This includes prevailing wage requirements, public

works requirements, and environmental building standards.

In contrast, market-rate projects have a simpler financing structure. Often a single

bank loan and an equity contribution can fund the development.

The construction process is similar for low-income and market-rate housing

development

The construction process is largely the same for both types of housing developments.

Both may use the same contractors, buy the same materials, and utilize the same labor

pool. They are subject to the same local regulations, such as design review and

permitting. All housing developments are subject to the same building codes and must

pass inspections. As noted above, when prevailing wages apply, there may be additional

compliance requirements.

State and federal rent caps limit future operating income for low-income

housing

Low-income housing projects are limited in their ability to raise operating income

because rent is restricted to levels set by federal and state agencies. The

restrictions are in place for 30 years or more. In addition, projects that serve

extremely low-income populations, such as supportive housing for the homeless, may

incur the cost of providing necessary tenant services. Due to these operating income

limits, investors may require and regulate the use of operating reserves by developers

to pay for future repairs or unexpected costs.

In contrast, developers of market-rate housing can adjust rents to market conditions

and use rental revenue for operating costs and profit.

Subsidized low-income developers have more sale restrictions

Sale or transfer of ownership of subsidized low-income housing developments are

subject to funding program approvals and procedures. Projects must comply with rent

restrictions for 30 years or more. Sale prices reflect the requirements for long-term

rental restrictions.

In contrast, market-rate developers can sell at any time at market price.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

Appendix A: Case studies

JLARC staff reviewed six case studies from the Low-Income Housing

Tax Credit program

JLARC staff selected six Low-Income Housing Tax Credit (LIHTC) developments for

analysis of the development process and costs. The case studies represent a variety of

LIHTC developer types and project sites. All projects were completed within the last

four years and many are intended for specific low-income populations, such as homeless

young adults, farmworkers, seniors, and people with disabilities. The six case studies

include:

Two from each funding region (Seattle/King County, Metro, and Non-Metro).

Two from each developer type (nonprofit, for-profit, and housing authority).

Three from each type of tax credit (9% tax credit and bond/4% tax credit).

JLARC's professional cost estimator calculated a retrospective cost estimate for each

housing development (tab

2). A second cost estimator reviewed the estimates and found them to be thorough

and reasonable. More details about each project are below.

Copper Landing, Airway Heights

Source: Photo courtesy of Inland Group.

Developer type: For-profit, vertically integrated

Developer name: Inland Group

LIHTC type: Bond/4% tax credit

Average tenant income: 53% of area median income (AMI)

Population served: Households earning 60% or below AMI

Number of units: 216

Year placed in service: 2014

Total development costs (millions): $22.7

Cost estimate range (millions): $26.8-$36.2

Wage requirement: Davis-Bacon (federal)

residential As required by the Davis-Bacon Act of

1931, federally funded construction projects must pay a minimum wage

determined by the US Department of Labor to laborers and mechanics. In

general, wage rates for residential construction are lower than wage rates

for non-residential construction.

Copper Landing is located on Kalispel Tribal Trust Land. The developer entered into a

ground lease agreement with the Kalispel tribe for the right to build on the property.

The development was financed using bond/4% tax credits and bank and business loans.

The development consists of nine buildings with one-, two-, and three-bedroom

garden-style walk-up apartments The development also has a clubhouse, playground, and

pool.

15 West, Vancouver

Source: Photo courtesy of DBG Properties LLC.

Developer type: For-profit, vertically integrated

Developer name: DBG Properties LLC

LIHTC type: Bond/4% tax credit

Average tenant income: 51% of area median income (AMI)

Population served: Households earning 60% or below AMI

Number of units: 120

Year placed in service: 2016

Total development costs (millions): $19.1

Cost estimate range (millions): $19.1-$25.8

Wage requirement: None

15 West was financed using bond/4% tax credits, loans, and developer equity. The

developer also received a multifamily tax exemption.A 12-year property tax exemption offered by cities to

qualifying projects that provide low-income housing. 15 West is a

mid-rise building with studio, one-, two-, and three-bedroom units. The units are

restricted to tenants who earn 60% or below the area median income.

Marion West, Seattle

Source: Photo courtesy of Low Income Housing Institute.

Developer type: Nonprofit

Developer name: Low Income Housing Institute

LIHTC type: 9% tax credit

Average tenant income: 30% of area median income (AMI)

Population served: 20 units reserved for homeless young adults, the

rest of the units are for households earning below 30%, 40% or 60% AMI

Number of units: 49

Year placed in service: 2014

Total development costs (millions): $15.1

Cost estimate range (millions): $12.4-$16.7

Wage requirement: State commercial By state law, construction contractors must pay

workers prevailing wages on state-funded projects. Wage rates are

established by the Department of Labor and Industries. In general,

commercial wage rates are higher than residential wage rates. A commercial

wage rate may be required on housing construction if there are

non-residential spaces (such as a food bank) in an otherwise residential

building.

Marion West, originally called University Commons, is a mixed-use building located in

Seattle's University District. The development was funded using 9% tax credits,

low-interest loans from the City of Seattle, King County, and the Housing Trust Fund,

developer equity, capital campaign proceeds, and the State Building Communities Fund.

The residential portion of the development has on-site caseworkers and full-time staff

and provides 47 studio and two one-bedroom units. The University District Food Bank is

located on the first floor and includes a nonprofit coffee shop that provides job

training for youth. There is a rooftop garden that supplements the food bank.

Rio de Vida, Prosser

Source: Photo courtesy of Office and Rural Farmworker Housing.

Developer type: Nonprofit

Developer name: Catholic Charities Housing Services of Yakima

LIHTC type: 9% tax credit

Average tenant income: 30% of area median income (AMI)

Population served: Units are reserved for households earning 30% or

50% AMI. 38 units are reserved for farmworkers.

Number of units: 51

Year placed in service: 2016

Total development costs (millions): $11.0

Cost estimate range (millions): $10.6-$14.4

Wage requirement: Mix of Davis-Bacon (federal)

As required by the Davis-Bacon Act of 1931,

federally funded construction projects must pay a minimum wage determined

by the US Department of Labor to laborers and mechanics. In general, wage

rates for residential construction are lower than wage rates for

non-residential construction. residential and

commercial

Rio de Vida, originally called Prosser Family Housing, is a 51-unit townhouse

development built by the Catholic Charities Housing Services Yakima with assistance

from the Office of Rural and Farmworker Housing. The development was funded using 9%

tax credits, low-interest loans from the United States Department of Agriculture Rural

Development, and Benton County 2060 funds. There are two- and three-bedroom units. The

development also features a common room, kitchen, recreation area, and computer

lab.

Vantage Point Apartments, Renton

Source: Photo courtesy of King County Housing Authority.

Developer type: Housing Authority

Developer name: King County Housing Authority

LIHTC type: 9% tax credit

Average tenant income: 18% of area median income (AMI)

Population served: Seniors or non-elderly disabled households earning

less than 30% or 50% of the AMI

Number of units: 77

Year placed in service: 2015

Total development costs (millions): $26.7

Cost estimate range (millions): $24.7-$33.4

Wage requirement: Davis-Bacon (federal)

residentialAs required by the Davis-Bacon Act of

1931, federally funded construction projects must pay a minimum wage

determined by the US Department of Labor to laborers and mechanics. In

general, wage rates for residential construction are lower than wage rates

for non-residential construction.

Vantage Point Apartments was developed by the King County Housing Authority (KCHA) on

an existing KCHA property. The development was financed using 9% tax credits, with

additional funds from the state, county, and developer. The KCHA developed the project

after it secured operating assistance from the Department of Housing and Urban

Development. The development has 77 units: 72 one-bedroom and 5 two-bedroom units.

Lariat Gardens, Walla Walla

Source: Photo courtesy of Walla Walla Housing Authority.

Developer type: Housing Authority

Developer name: Walla Walla Housing Authority

LIHTC type: Bond/4% tax credit

Average tenant income: 23% of area median income (AMI)

Population served: Households earning 60% or below AMI

Number of units: 43

Year placed in service: 2015

Total development costs (millions): $8.2

Cost estimate range (millions): $7.5-$10.2

Wage requirement: State residentialBy state law, construction contractors must pay

workers prevailing wages on state-funded projects. Wage rates are

established by the Department of Labor and Industries. In general,

residential wage rates are lower than commercial wage rates.

Originally a motel built in 1961, Lariat Gardens was converted into housing in 2001.

The Walla Walla Housing Authority (WWHA) acquired the site in 2009 to preserve

affordable housing near the downtown core. The WHHA renovated the existing building

and constructed new buildings. The development was financed using bond/4% tax credits,

low-interest loans from the Housing Trust Fund, HUD HOME funds, and developer equity.

Lariat Gardens has 43 units: 23 one-bedroom and 20 two-bedroom.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Report Details

Appendix B: Detailed statistical analysis

Regression analysis identified variables associated with changes

in development costs

JLARC staff conducted linear regression analysis to identify how certain factors

affect the costs of developing low-income housing. The model included 241 low-income

housing projects financed using Low-Income Housing Tax Credits (LIHTC) that were

placed in service in the period 2010-2017.

What is regression analysis?

Regression analysis is a statistical technique used to estimate the quantitative

relationships between multiple factors (independent variables) and a particular

outcome (dependent variable). For example, regression analysis can measure how a

building's size affects its development costs. When there are many factors that affect

an outcome, researchers can use regression to "control for," or take into

consideration, those other factors. In this case, regression analysis can measure how

a building's size affects its development costs while separately taking into

consideration other factors such as the building's location, and its developer type.

Regression analysis estimates the variance accounted for in the outcome given the

independent variables. The outcome is called the "dependent variable." In this study,

JLARC staff conducted several regression analyses using different dependent variables,

including a project's total development cost (TDC) per unit, TDC per square foot, and

TDC per bedroom. Ultimately, we decided to use TDC per bedroom for three reasons:

The regression analysis with TDC per bedroom was generally consistent with other

models and showed the greatest explanatory power of all the dependent variables we

considered.

TDC per bedroom serves as a reasonable proxy for the number of people served by

low-income housing programs as compared to per unit or per square foot.

A regression analysis of TDC per bedroom offers a unique contribution to research

on low-income housing development costs.

Most studies do not analyze TDC per bedroom because adequate data is rarely

available. To make our research accessible to researchers that use TDC per unit, we

have also included our regression analysis of TDC per unit and TDC per square foot

below.

We also developed a series of regression models based on different regions of the

state (King County, Metro, and Non-Metro areas). These models are generally consistent

with the initial models, so for the sake of brevity the models are not displayed in

this appendix.

Source data

Data for the regression analyses came primarily from two sources: the Washington

State Housing Finance Commission (WSHFC) and the U.S. Census.

WSHFC: LIHTC Project Data - WSHFC provided JLARC staff with project cost data

for Low-Income Housing Tax Credit (LIHTC) projects placed in service between 2010 and

early 2017. This is the most recent data available. WSHFC staff indicated that the

most reliable sources of cost data for LIHTC projects are the cost certifications that

all projects must submit, pursuant to requirements from the Internal Revenue

Service. JLARC staff received final cost certifications for 241 LIHTC projects,

compiled this data, and developed additional variables based on this data (see

Neighborhood Characteristic Data).

U.S. Census: Neighborhood Characteristic Data - JLARC staff compiled selected

characteristic data for the census tracts in which LIHTC projects are located. These

data include the median contract rent, the median housing stock age, and the

percentage of the population with income below the poverty line for the years in which

the project applied for the LIHTC allocation.

The final analyses use the characteristic data from the application year, rather than

the placed-in-service year, because these variable are a reasonable proxy for property

values and infrastructure condition prior to the start of construction. If the model

had used data from the year the LIHTC projects were placed in service, potential

improvements from the LIHTC development to the neighborhood could have biased the

estimates.

Dependent variables

JLARC staff considered multiple model specifications to assess the relationship

between project characteristics and inflation-adjusted total development cost (TDC)

per bedroom, per unit, and per square foot.

The TDC calculation does not include land acquisition and reserves. JLARC staff

omitted land cost from total development costs because it varies widely due to

geography and other factors that are extraneous to housing development. Doing

otherwise could offer a misleading comparison of development costs. In some cases,

land may be donated, leased, or acquired at below market rates. For example, in one

project a nonprofit developer acquired a 0.8 acre property in Redmond for $75. At the

time of the acquisition, a neighboring property of nearly identical size had an

appraised land value of nearly $2 million.

JLARC staff also omitted reserve amounts because they, too, could offer a misleading

comparison of development costs. Reserves are not uniformly required of all LIHTC

projects. Lenders, investors, or public funders may decide whether a reserve is

required and establish the amount.

Since projects were built in different years, JLARC staff adjusted development costs

for inflation. JLARC staff used the chained price deflator for multi-family

residential construction estimated by IHS-Global Insight to index the construction

costs to 2017.

The data included some projects with per-bedroom development costs well above those

of most other projects. JLARC staff statistically adjusted for the skew caused by

these projects by calculating the logarithm of the development costs. This is a

typical technique to adjust for a skewed population in regression analysis methods.

Regression coefficients are typically interpreted as a unit change in an independent

variable being associated with a unit change in the dependent variable. However, the

log transformation of the original dependent-variable data requires a conversion of

the regression coefficients such that the interpretation of each unit change in the

independent variable is associated with a percent change in the dependent

variable.

Exhibit B1: Distribution of total development cost by developer type

Click on image to enable interactive data filtering (clicking on image will take you

to another website called Tableau Public).

Exhibit B2: Descriptive statistics of the dependent variables for the regression

models

Dependent Variable

Mean

Median

Standard Deviation

Range

Minimum

Maximum

Count

Natural log of TDC minus land and reserves per bedroom

11.8

11.7

0.5

1.9

10.9

12.8

241

Natural log of TDC minus land and reserves per unit

12.3

12.3

0.3

2.0

11.2

13.2

241

Natural log of TDC minus land and reserves per square foot

5.4

5.4

0.4

2.0

4.6

6.6

241

Source: JLARC staff statistical analysis of LIHTC data.

Independent variables

JLARC staff identified independent variables based on a review of existing research

and interviews with stakeholders. Explanations of the independent variables used in

the regression are below and the descriptive statistics are displayed in Exhibit B2.

Many of the independent variables are binary. These variables have a value of 1 if the

condition they describe is true, and the value is 0 if the condition does not apply.

The neighborhood characteristics variables were created using the U.S. Census’

American Community Survey data.

Construction years are seven binary variables for the respective years 2009-2016.

Construction year is an estimated value and defined as the year prior to a project

being placed in service. In the analysis, 2015 is omitted and serves as the

comparison category for each included year.

Two binary variables capture developer type and identify projects as having been

developed by nonprofit or government entities. For-profit developers are factored

into the analysis by serving as the comparison category.

Two binary regional variables capture projects located in King County or Metro areasThe Commission divides the

state into three geographic regions: Seattle/King County, Metro (Clark, Pierce,

Snohomish, Spokane, and Whatcom counties), and Non-Metro (all other

counties).. The comparison category is for projects located in

Non-Metro areas.

New construction is a binary variable identifying new construction projects.

Rehabilitation projects are the comparison category.

9% tax credit LIHTC is a binary variable identifying developments participating in

the 9% tax credit program and bond/4% tax credit program. The bond/4% tax credit

program is the comparison category.

Number of units captures the total number of units built for each LIHTC

development.

Average square foot per unit captures the average square footage of residential

space, common areas, and structured parking per unit in the LIHTC development.

Average number of bedrooms per unit provides an alternate measure of unit size for

each LIHTC development. This variable also allows for estimates of the number of

people potentially served by each development.

Four stories or more is a binary variable indicating whether each project is four

stories or more. This variable was estimated by counting the projects that listed

mid- or high-rise units on the cost certifications, rather than single-family,

townhouse, or walk-up units.

Structured parking is a binary variable identifying housing developments that

included any structured parking stalls.

Vertical integration is a binary variable identifying whether the developer was

vertically integrated for the project. Vertical

integration means the developer also serves as their own general contractor or has

a shared interest with the project's general contractor. JLARC staffed

relied on information included in the cost certification documents to identify

developments where the developer also served as the general contractor.

Homeless units is a binary variable identifying whether the project has any units

dedicated for people experiencing homelessness.

Median contract rent is a continuous variable identifying the median rent in the

census tract where the project is located, in the year in which the application for

the LIHTC was submitted.

Median housing stock age is a continuous variable identifying the age of the

neighborhood housing in the year the application for the LIHTC was submitted. The

variable was estimated as the difference between the application year and the median

build year.

Percent below poverty is a continuous variable identifying the percentage of

individuals with income below the poverty line in the year the application for LIHTC

was submitted.

Exhibit B3: Descriptive statistics of independent variables for the regression

models

Descriptive Statistics - Independent Variables

Mean

Median

Standard Deviation

Range

Minimum

Maximum

Count

2009 construction year

0.09

0.00

0.29

1

0

1

241

2010 construction year

0.14

0.00

0.34

1

0

1

241

2011 construction year

0.10

0.00

0.31

1

0

1

241

2012 construction year

0.15

0.00

0.35

1

0

1

241

2013 construction year

0.15

0.00

0.35

1

0

1

241

2014 construction year

0.17

0.00

0.38

1

0

1

241

2015 construction year

0.20

0.00

0.40

1

0

1

241

2016 construction year

0.01

0.00

0.09

1

0

1

241

Nonprofit

0.48

0.00

0.50

1

0

1

241

For-profit

0.23

0.00

0.42

1

0

1

241

Government

0.29

0.00

0.45

1

0

1

241

Vertical integration

0.20

0.00

0.40

1

0

1

241

King County

0.32

0.00

0.47

1

0

1

241

Metro

0.33

0.00

0.47

1

0

1

241

Non-metro

0.35

0.00

0.48

1

0

1

241

New construction

0.65

1.00

0.48

1

0

1

241

Rehabilitation of existing building

0.35

0.00

0.48

1

0

1

241

Bond/4% tax credit

0.49

0.00

0.50

1

0

1

241

9% tax credit program

0.51

1.00

0.50

1

0

1

241

Number of units

87.98

60.00

75.92

439

10

449

241

Avg. beds per unit

1.8

1.7

0.7

3

1

4

241

Residential square feet per unit

963

949

302

2,847

252

3,099

241

4 or more stories

0.3

0.00

0.5

1

0

1

241

Structured parking

0.2

0.00

0.4

1

0

1

241

Homeless units

0.2

0.00

0.4

1

0

1

241

Median contract rent (App. Yr.)

$980

$951

$327

$1,891

$195

$2,086

241

Median housing stock age (App. Yr.)

43.2

42.0

16.6

64

14

78

241

% Individuals below poverty line (App. Yr.)

21.5%

20.3%

11.9%

52.3%

1.0%

53.2%

241

Source: JLARC staff statistical analysis of LIHTC and U.S. Census data.

A correlation matrix showing the bivariate associations between each of the

independent variables is located here.

Results

The model with the most explanatory power used the natural logarithm of total

development cost (TDC) per bedroom, excluding reserves and land costs. The adjusted

r-squared statistic is 0.765 and represents the amount of variation in the dependent

variable that is accounted for by the full regression model. The regression analysis

showed the following independent variables had a statistically significant

relationship to development cost:

Nonprofit – predicts an average cost increase of 15 percent compared to

for-profit developers.

Government Housing Authority – predicts an average cost increase of 28

percent compared to for-profit developers.

King County – predicts an average cost increase of 23 percent compared to

Non-Metro counties.

New construction – predict an average cost increase of 31 percent compared

to rehabilitation projects.

Number of units – predicts an average cost reduction of 0.1 percent per

bedroom for each additional unit. This likely reflects economies of scale for

development with more units.

Average bedrooms per unit – predicts an average cost reduction of 31

percent per bedroom for each one-bedroom increase in the average number of bedrooms

per unit. This likely reflects economies of scale for developments with more

bedrooms per unit.

Vertical integration – predicts an average cost reduction of 11 percent

compared to developments run by non-vertically integrated developers.

Median contract rent – predicts an average 0.03 percent cost increase per

bedroom for each $1 increase in rent.

Median housing stock age – each one-year increase in the age of housing

stock predicts a 0.4 percent increase in the per bedroom cost.

Percent individuals below poverty line – predicts an average 0.5 percent increase

in the per bedroom cost for each percentage-point increase in the poverty

rate.

Other dependent variables were not statistically significant predictors of total

development cost. Full model results are shown in Exhibit B3.

Exhibit B4: Regression model results - inflation-adjusted TDC (minus land &

reserves) per bedroom, natural log

Source: JLARC staff statistical analysis of LIHTC and U.S. Census data.

Total development cost (excluding land and reserves) per unit

Other studies of LIHTC development costs use the total development cost (TDC) per

unit as their dependent variable, including reports by the Government Accountability

Office, the National Council of State Housing Agencies (prepared by Abt Associates),

Jean Cummings and Denise Di Pasquale (economists who conducted the first major

regression analysis on LIHTC development costs for City Research, an urban economics

consulting firm, and formerly affiliated with the Joint Center for Housing Studies at

Harvard University), and the state of California (prepared by Blue Sky Consulting). In

order to compare our findings with this other research, JLARC staff conducted a

regression analysis using the TDC per unit. Although there is some variation in model

specifications, JLARC staff findings are generally consistent with other research,

including the findings regarding developer type, economies of scale, and neighborhood

characteristics. The adjusted r-squared statistic indicates that this model

specification accounts for 59 percent of the variance in the natural logarithm of the

TDC per unit.

Exhibit B5: Regression results - inflation adjusted TDC (excluding land &

reserves) per unit, natural log

Source: JLARC staff statistical analysis of LIHTC and U.S. Census data.

Total development cost (less land and reserves) per square foot

JLARC staff also analyzed costs on a square foot basis. Results are similar to the

per unit model, but with less explanatory power than the per bedroom model used in the

report.

Exhibit B6: Regression results - inflation adjusted TDC (excluding land &

reserves) per square foot, natural log

Source: JLARC staff statistical analysis of LIHTC and U.S. Census data.

JLARC staff interpret the regression results to be robust as all three models show

similar patterns in the estimated relationships between the independent variables and

each respective dependent variable. While the magnitude of the relationships (measured

as the percent change) between each independent variable and different measures of the

total development cost depends on the model specifications, the overall pattern is

consistent using this data.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

Except as provided in this section, affordable housing projects funded out of the

state capital budget are exempt from the provisions of this chapter. On or before July

1, 2008, the *department of community, trade, and economic development shall identify,

implement, and apply a sustainable building program for affordable housing projects

that receive housing trust fund (under chapter 43.185 RCW) funding in a state capital

budget. The *department of community, trade, and economic development shall not

develop its own sustainable building standard, but shall work with stakeholders to

adopt an existing sustainable building standard or criteria appropriate for affordable

housing. Any application of the program to affordable housing, including any

monitoring to track the performance of either sustainable features or energy standards

or both, is the responsibility of the *department of community, trade, and economic

development. Beginning in 2009 and ending in 2016, the *department of community,

trade, and economic development shall report to the department as required under RCW

39.35D.030(3)(b).

[ 2005 c 12 § 12.]

NOTES:

*Reviser's note: The "department of community, trade, and economic

development" was renamed the "department of commerce" by 2009 c 565.

Use of moneys for loans and grant projects to provide housing—Eligible

activities.

RCW 43.185.050

(1) The department must use moneys from the housing trust fund and other legislative

appropriations to finance in whole or in part any loans or grant projects that will

provide housing for persons and families with special housing needs and with incomes

at or below fifty percent of the median family income for the county or standard

metropolitan statistical area where the project is located. At least thirty percent of

these moneys used in any given funding cycle must be for the benefit of projects

located in rural areas of the state as defined by the department. If the department

determines that it has not received an adequate number of suitable applications for

rural projects during any given funding cycle, the department may allocate unused

moneys for projects in nonrural areas of the state.

(2) Activities eligible for assistance from the housing trust fund and other

legislative appropriations include, but are not limited to:

(a) New construction, rehabilitation, or acquisition of low and very low-income

housing units;

(b) Rent subsidies;

(c) Matching funds for social services directly related to providing housing for

special-need tenants in assisted projects;

(d) Technical assistance, design and finance services and consultation, and

administrative costs for eligible nonprofit community or neighborhood-based

organizations;

(e) Administrative costs for housing assistance groups or organizations when such

grant or loan will substantially increase the recipient's access to housing funds

other than those available under this chapter;

(f) Shelters and related services for the homeless, including emergency shelters and

overnight youth shelters;

(g) Mortgage subsidies, including temporary rental and mortgage payment subsidies to

prevent homelessness;

(h) Mortgage insurance guarantee or payments for eligible projects;

(i) Down payment or closing cost assistance for eligible first-time home buyers;

(j) Acquisition of housing units for the purpose of preservation as low-income or

very low-income housing;

(k) Projects making housing more accessible to families with members who have

disabilities; and

(l) Remodeling and improvements as required to meet building code, licensing

requirements, or legal operations to residential properties owned and operated by an

entity eligible under RCW 43.185A.040, which were transferred as described in RCW

82.45.010(3)(t) by the parent of a child with developmental disabilities.

(3) Preference must be given for projects that include an early learning facility.

(4) Legislative appropriations from capital bond proceeds may be used only for the

costs of projects authorized under subsection (2)(a), (i), and (j) of this section,

and not for the administrative costs of the department.

(5) Moneys from repayment of loans from appropriations from capital bond proceeds may

be used for all activities necessary for the proper functioning of the housing

assistance program except for activities authorized under subsection (2)(b) and (c) of

this section.

(6) Administrative costs associated with application, distribution, and project

development activities of the department may not exceed three percent of the annual

funds available for the housing assistance program. Reappropriations must not be

included in the calculation of the annual funds available for determining the

administrative costs.

(7) Administrative costs associated with compliance and monitoring activities of the

department may not exceed one-quarter of one percent annually of the contracted amount

of state investment in the housing assistance program.

[ 2018 c 223 § 4; 2017 3rd sp.s. c 12 § 13; 2013 c 145 § 2; 2011 1st sp.s. c 50 §

953; 2006 c 371 § 236. Prior: 2005 c 518 § 1801; 2005 c 219 § 1; 2002 c 294 § 6; 1994

c 160 § 1; 1991 c 356 § 4; 1986 c 298 § 6.]

NOTES:

Findings—2018 c 223: See note following RCW 82.45.010.

Findings—Intent—Effective date—2017 3rd sp.s. c 12: See notes following RCW

43.31.565.

Effective dates—2011 1st sp.s. c 50: See note following RCW 15.76.115.

Effective date—2006 c 371: See note following RCW 27.34.330.

Severability—Effective date—2005 c 518: See notes following RCW 28A.500.030.

Findings—2002 c 294: See note following RCW 36.22.178.

Notice of grant and loan application period—Priorities—Criteria for evaluation.

RCW 43.185.070

(1) During each calendar year in which funds from the housing trust fund or other

legislative appropriations are available for use by the department for the housing

assistance program, the department must announce to all known interested parties, and

through major media throughout the state, a grant and loan application period of at

least ninety days' duration. This announcement must be made as often as the director

deems appropriate for proper utilization of resources. The department must then

promptly grant as many applications as will utilize available funds less appropriate

administrative costs of the department as provided in RCW 43.185.050.

(2) In awarding funds under this chapter, the department must:

(a) Provide for a geographic distribution on a statewide basis; and

(b) Until June 30, 2013, consider the total cost and per-unit cost of each project

for which an application is submitted for funding under RCW 43.185.050(2) (a) and (j),

as compared to similar housing projects constructed or renovated within the same

geographic area.

(3) The department, with advice and input from the affordable housing advisory board

established in RCW 43.185B.020, or a subcommittee of the affordable housing advisory

board, must report recommendations for awarding funds in a cost-effective manner. The

report must include an implementation plan, timeline, and any other items the

department identifies as important to consider to the legislature by December 1, 2012.

(4) The department must give first priority to applications for projects and

activities which utilize existing privately owned housing stock including privately

owned housing stock purchased by nonprofit public development authorities and public

housing authorities as created in chapter 35.82 RCW. As used in this subsection,

privately owned housing stock includes housing that is acquired by a federal agency

through a default on the mortgage by the private owner. Such projects and activities

must be evaluated under subsection (5) of this section. Second priority must be given

to activities and projects which utilize existing publicly owned housing stock. All

projects and activities must be evaluated by some or all of the criteria under

subsection (5) of this section, and similar projects and activities shall be evaluated

under the same criteria.

(5) The department must give preference for applications based on some or all of the

criteria under this subsection, and similar projects and activities must be evaluated

under the same criteria:

(a) The degree of leveraging of other funds that will occur;

(b) The degree of commitment from programs to provide necessary habilitation and

support services for projects focusing on special needs populations;

(c) Recipient contributions to total project costs, including allied contributions

from other sources such as professional, craft and trade services, and lender interest

rate subsidies;

(d) Local government project contributions in the form of infrastructure

improvements, and others;

(e) Projects that encourage ownership, management, and other project-related

responsibility opportunities;

(f) Projects that demonstrate a strong probability of serving the original target

group or income level for a period of at least twenty-five years;

(g) The applicant has the demonstrated ability, stability and resources to implement

the project;

(h) Projects which demonstrate serving the greatest need;

(i) Projects that provide housing for persons and families with the lowest incomes;

(j) Projects serving special needs populations which are under statutory mandate to

develop community housing;

(k) Project location and access to employment centers in the region or area;

(l) Projects that provide employment and training opportunities for disadvantaged

youth under a youthbuild or youthbuild-type program as defined in RCW 50.72.020;

(m) Project location and access to available public transportation services; and

(n) Projects involving collaborative partnerships between local school districts and

either public housing authorities or nonprofit housing providers, that help children

of low-income families succeed in school. To receive this preference, the local school

district must provide an opportunity for community members to offer input on the

proposed project at the first scheduled school board meeting following submission of

the grant application to the department.

(6) The department may only approve applications for projects for persons with mental

illness that are consistent with a behavioral health organization six-year capital and

operating plan.

[ 2015 c 155 § 2; (2015 c 155 § 1 expired April 1, 2016); 2014 c 225 § 62; 2013 c 145

§ 3; 2012 c 235 § 1. Prior: 2005 c 518 § 1802; 2005 c 219 § 2; 1994 sp.s. c 3 § 9;

prior: 1991 c 356 § 5; 1991 c 295 § 2; 1988 c 286 § 1; 1986 c 298 § 8.]

NOTES:

Effective date—2015 c 155 § 2: "Section 2 of this act takes effect April 1, 2016." [

2015 c 155 § 4.]

Expiration date—2015 c 155 § 1: "Section 1 of this act expires April 1, 2016." [ 2015

c 155 § 3.]

Effective date—2014 c 225: See note following RCW 71.24.016.

Severability—Effective date—2005 c 518: See notes following RCW 28A.500.030.

Application process—Distribution procedure.

RCW 43.185.130

The application process and distribution procedure for the allocation of funds are

the same as the competitive application process and distribution procedure for the

housing trust fund, described in this chapter and chapter 43.185A RCW, except for the

funds applied to the *homeless families services fund created in RCW 43.330.167,

dollars appropriated to weatherization administered through the energy matchmaker

program, dollars appropriated for housing vouchers for homeless persons, victims of

domestic violence, and low-income persons or seasonal farmworkers, and dollars

appropriated to any program to provide financial assistance for grower-provided

on-farm housing for low-income migrant or seasonal farmworkers.

[ 2006 c 349 § 3.]

NOTES:

*Reviser's note: The "homeless families services fund" was renamed the "Washington

youth and families fund" by 2015 c 69 § 24.

Finding—2006 c 349: "The legislature finds that Washington is experiencing an

affordable housing crisis and that this crisis is growing exponentially every year as

the population of the state expands and housing values increase at a rate that far

exceeds most households' proportionate increase in income.

The fiscal and societal costs of the lack of adequate affordable housing are high for

both the public and private sectors. Current levels of funding for affordable housing

programs are inadequate to meet the housing needs of many low-income Washington

households." [ 2006 c 349 § 1.]

Affordable Housing Program

RCW 43.185A.010

Definitions.

Unless the context clearly requires otherwise, the definitions in this section apply

throughout this chapter.

(1) "Affordable housing" means residential housing for rental occupancy which, as

long as the same is occupied by low-income households, requires payment of monthly

housing costs, including utilities other than telephone, of no more than thirty

percent of the family's income. The department must adopt policies for residential

homeownership housing, occupied by low-income households, which specify the percentage

of family income that may be spent on monthly housing costs, including utilities other

than telephone, to qualify as affordable housing.

(2) "Contracted amount" has the same meaning as provided in RCW 43.185.020.

(3) "Department" means the department of commerce.

(4) "Director" means the director of the department of commerce.

(5) "First-time home buyer" means an individual or his or her spouse or domestic

partner who have not owned a home during the three-year period prior to purchase of a

home.

(6) "Low-income household" means a single person, family or unrelated persons living

together whose adjusted income is less than eighty percent of the median family

income, adjusted for household size, for the county where the project is located.[ 2013 c 145 § 4; 2009 c 565 § 38; 2008 c 6 § 301; 2000 c 255 § 9; 1995 c 399 § 102; 1991 c 356 § 10.]

NOTES:

Part headings not law—Severability—2008 c 6: See RCW 26.60.900 and 26.60.901.

Effective date—2000 c 255: See RCW

59.28.902.

19-02 Final Report | Analyzing Development Costs for Low-Income Housing

January 2019

Recommendations & Responses

Legislative Auditor Recommendation

The Legislative Auditor makes 3 recommendations to improve cost

efficiency, controls, and monitoring

Recommendation #1: The Commission should identify and evaluate options for

increasing the involvement of for-profit developers in the 9% tax credit program and

report their findings to the Legislature.

There are a variety of options the Commission could evaluate for increasing the

involvement of for-profit developers in the 9% tax credit program. The Commission

currently engages for-profit developers in the bond/4% tax credit program and there

may be lessons learned from this experience that can apply to the 9% tax credit

program.

Legislation Required:

None

Fiscal Impact:

JLARC staff assume the Commission can identify and evaluate options within

existing resources

Recommendation #2: Commerce should collect final development cost data from Housing

Trust Fund recipients to improve cost controls.

Commerce should implement procedures to collect final development cost data. Commerce

may coordinate with other public funders to receive copies of certified final

development costs. It should use this data to implement its 2012 recommendation to

document and monitor development cost data over time. It should also use this data to

inform their cost containment policy.

Legislation Required:

None

Fiscal Impact:

JLARC staff assume Commerce can implement data collection procedures within

existing resources

Recommendation #3: Commerce and the Commission should report development cost data

to the Legislature annually.

Data should include the total development cost per unit for each project, descriptive

statistics (such as average and median per unit costs), regional cost variation, and

other cost data that agencies deem necessary to improve cost controls and enhance the

Legislature's understanding of development costs. Commerce and the Commission should

coordinate to identify relevant development cost data and ensure that measures are

consistent across the agencies. The costs should be published in a format that allows

the Legislature and the agencies to track development costs over time.

Legislation Required: