The aerospace industry remains in Washington, offering wages and

benefits above the state average. The preferences improved competitiveness by reducing

the industry's effective tax rate by 50%. Employment has declined from its 2013 level,

but it is unclear to what extent the preferences prevented greater job loss.

Review focuses on nine tax preferences intended to benefit the aerospace

industry

In 2013, the Legislature expanded a package of aerospace tax

preferences that was initially enacted in 2003. The preferences include three

preferential business and occupation (B&O) tax rates, two B&O tax

credits, two sales and use tax exemptions, a property tax exemption, and a

leasehold excise tax exemption. Detail is provided in Appendix A.

To claim a preference, a business must perform at least one of these

activities:

Manufacture commercial airplanes.

Develop aerospace products (e.g., airplanes, components, repair equipment,

and tooling).

Repair aircraft.

The preferences are scheduled to expire July 1, 2040.

Estimated Biennial Beneficiary Savings

$569 million in the 2021-23 Biennium

Tax Types

Business and Occupation Tax, Sales and Use Tax, Leasehold Excise Tax,

Property Tax

The preferences lower the cost of doing business. The aerospace industry remains

in Washington, and its employees earn wages above the state average and are provided

benefits.

The Legislature stated three public policy objectives when the preferences were

initially enacted in 2003, and added a fourth policy objective when extending the

preferences in 2013.

Objectives (Stated)

Results

Reduce the cost of doing business in Washington for the aerospace

industry compared to other states.

Met. The preferences save beneficiaries more than $500 million per

biennium. They improve the state’s competitive position by cutting the

industry’s effective tax rate by at least 50%, making the rate lower than 5

out of 13 competitor states. (Tab 1)

Encourage the continued presence of the aerospace industry in

Washington.

Met. Aerospace continues to be a major industry in Washington.

However, it is unclear to what extent the preferences influenced location

decisions. (Tab 2)

Provide jobs with good wages and benefits.

Met. Aerospace industry employees earn wages and benefits well above

the state average. (Tab 3)

However, aerospace employment is lower than it was in 2013. It is unclear whether

the preferences prevented greater job losses.

Objectives (Stated)

Results

Maintain and grow Washington's aerospace industry workforce.

Unclear. Washington aerospace employment is lower than it was in

2013, but higher than when the preferences were first enacted in 2003. (Tab 3) If the preferences led Boeing to remain in Washington,

they may have kept the state from losing more jobs. If not, they reduced

government spending and may have contributed to job losses. (Tab 4)

Recommendations

Legislative Auditor's Recommendation: Clarify

The Legislature should clarify its expectations for the level of aerospace industry

employment. Providing additional detail in the tax preference performance statement

such as a baseline level of employment would facilitate future reviews of these

preferences.

1. Preferences reduce costs and improve competitiveness

The preferences improved Washington's competitive position by

cutting the industry’s effective tax rate by at least 50%

Over 600 beneficiaries have claimed seven of nine preferences

In 2003, the Legislature approved a package of aerospace tax preferences. In 2013, it

extended the preferences' expiration date from 2024 to 2040. The preferences

include:

Three preferential business and occupation (B&O) tax rates.

Two B&O tax credits.

Two sales and use tax exemptions (expanded in 2013).

One property tax exemption (unclaimed).

One leasehold excise tax exemption (unclaimed).See Appendix A for details.

The tax preferences reduce the cost of doing business for the aerospace industry and

other beneficiaries

A business may claim one or more of these preferences if it manufactures commercial

airplanes, develops aerospace productsAirplanes, airplane components, airplane repair equipment, and tooling used in

manufacturing commercial airplanes, or repairs aircraft. Businesses

in the aerospace industry were the primary beneficiaries, although firms in related

industries also claim the preferences.

The aerospace industry includes businesses that file taxes under North American

Industry Classification System (NAICS) code 3364--Aerospace Product and Parts

Manufacturing. Boeing is the largest aerospace business in Washington, and the

state's largest private employer.

Related industries include architectural and engineering services, durable goods

wholesaling, and fabricated metal product manufacturing.

From fiscal year 2014 through fiscal year 2017, 664 businesses saved $1.1 billion by

claiming the preferences. Beneficiaries in the aerospace industry claimed 93% of the

savings. Detailed savings estimates for each preference are in Appendix

A.

Exhibit 1.1: Beneficiaries save more than $500 million per biennium

Biennium

Fiscal Year

Estimated Fiscal Year Beneficiary Savings

Estimated Biennial Beneficiary Savings

2013-2015

7/1/13-6/30/15

2014

$223 million

$528 million

2015

$305 million

2015-2017

7/1/15-6/30/17

2016

$304 million

$543 million

2017

$239 million

2017-2019

7/1/17-6/30/19

2018

$246 million

$501 million

2019

$255 million

2019-2021

7/1/19-6/30/21

2020

$267 million

$545 million

2021

$278 million

2021-2023

7/1/21-6/30/23

2022

$282 million

$569 million

2023

$287 million

Source: JLARC staff analysis of tax return data - total savings may not equal sum of

detailed estimates due to rounding.

Independent consultant's tax accounting analysis concludes that the preferences

improved Washington’s competitiveness relative to other states

Four steps in Ernst & Young analysis to evaluate business tax climate

Estimate the rates of return and all taxesIncluding all state and local taxes a business may

pay, including sales, property, and B&O or income tax as

applicable paid by hypothetical small and large

aerospace firms that invest in new manufacturing facilities.

Estimate the reduction in rate of return due to taxes. As shown in the

hypothetical example below, the reduction due to taxes is the difference

between the pre-tax and after-tax rates of return.

Express the reduction as an effective tax rate.

Estimate the reduction in ETR due to statutory

incentivesExamples: preferential B&O

rates, sales and use tax exemptions and negotiated incentivesExamples:

tax abatements, cash grants. If incentives reduce taxes

in the above example by half, the effective tax rate would be reduced to

10%.

JLARC staff hired Ernst & Young to evaluate the business tax climate for the

aerospace industry across Washington and 13 other benchmark states. Benchmark states

include those with the highest concentration of aerospace employment and those

identified as leading states by recent studies of aerospace competitiveness. The

analysis considers statutory incentives (including Washington's aerospace tax

preferences), negotiated incentives, and cash grants provided to the aerospace

industry. Appendix

B has additional detail about the analysis and a link to the full report.

According to the analysis:

For the hypothetical large firmA

firm with 10,000 employees, the incentives reduce the effective

tax rate from 20.9% to 10.0%. This improves the state's competitive ranking from

thirteenth to ninth out of 14 states with a large aerospace presence (see Exhibit

1.2).

For the small firmA firm with 50

employees, the incentives reduce the effective tax rate from 15.8%

to 6.1%. This improves the state's competitive ranking from eleventh to eighth place

(see Appendix B).

In Washington, statutory incentives reduce the effective tax rate more than

negotiated incentives. Other states use more negotiated incentives.

For this study, the effective tax rate (ETR) includes all state and local taxes a

business may pay, including sales, property, and B&O or income tax as

applicable.

Washington's statutory incentives lower the ETR for large firms by 9.4 percentage

points (from 20.9% to 11.5%). Negotiated incentives reduce the ETR another 1.5

percentage points – from 11.5% to 10.0%. Cash grants are prohibited by the state

constitution.

Several of the benchmark states offer significant negotiated incentives and cash

grants that enhance their competitiveness compared to Washington.

When only statutory incentives are applied, Washington ranks fourth out of the 14

states for large firms.

When all types of incentives are considered, Washington places ninth for large

firms.

Exhibit 1.2: Washington's tax preferences improve its tax competitiveness

Note: Post-incentive ETR includes statutory incentives, negotiated incentives, and

cash grants.

Source: Ernst & Young analysis.

Preliminary Report | Aerospace Tax Preferences

Updated August 21, 2019

REVIEW Details

2. Aerospace remains a major Washington industry

Aerospace continues to be a major industry in Washington.

However, it is unclear to what extent the preferences influenced location

decisions.

Economic and employment data show that the aerospace industry has continued its

presence in Washington

BEA aggregates industries when measuring gross domestic product

The aerospace industry includes businesses that file taxes under North

American Industry Classification System (NAICS) code 3364--Aerospace Product

and Parts Manufacturing.

Other Transportation Equipment Manufacturing includes the

aerospace NAICS group and three other industry groups related to the

manufacture of railroad rolling stock, ships and boats, and other

transportation equipment.

Data from the Bureau of Economic Analysis (BEA) indicates that:

Nationally, the Other Transportation Equipment Manufacturing industry,

which includes aerospace, contributed $148 billion to the gross domestic product

in 2017. Washington's contribution – $32.4 billion – was 22% of the national total

and more than any other state.

In the 4th quarter of 2018, 198 businesses in the Aerospace Products and Parts

Manufacturing industry (NAICS 3364) employed 85,900 workers in Washington.

Although employment has declined in recent years (see Tab

3), it continues to be larger than in any other state, representing 17% of

national industry employment.

The concentration of aerospace value and jobs in Washington (location quotient)A location quotient measures the

concentration of a given industry in a given place relative to a larger region

such as the nation is greater than the national average. In 2017,

the value of goods and services made by Washington's Other Transportation

Equipment Manufacturing industry, as a portion of the state's economy, was 8.2

times greater than the national average. In 2018, the relative concentration of

aerospace industry jobs in the state was 7.3 times the national average.

Exhibit 2.1: Washington's aerospace industry leads nation in contribution to GDP and

industry employment

Source: Bureau of Economic Analysis, Bureau of Labor Statistics.

On average, beneficiaries provide wages and benefits that meet or exceed state

averages

The preferences aim to provide "good wages and benefits." Since these terms are not

defined, JLARC staff compared wage and benefit data for preference beneficiaries to

data from Washington's manufacturing industry in general.

Washington's average annual wage for manufacturing is just over $76,000. It is

$62,000 for all industries.

Beneficiaries of the aerospace tax preferences reported to the Department of

Revenue (DOR) that 72% of their employees earned more than $30 per hour (about

$62,000 annually) in 2017, and that more than 90% of employees are enrolled in

medical, dental, and retirement plans.

Employment Security Department (ESD) data shows that between 2016 and 2017,

beneficiaries paid employees an average annual wage greater than $100,000.

This data is consistent with information from the Bureau of Labor Statistics (BLS).

According to BLS, aerospace industry businesses in Washington paid a total of $9.5

billion in wages in 2017, averaging $114,000 per employee. The average annual wage is

the fourth highest of any state in the country for the industry and is above the U.S.

average aerospace wage of $101,000.

Exhibit 2.2: Beneficiaries paid employees more than $108,000 per year in 2017

Source: JLARC analysis of ESD Data, DOR Tax Return Data, BLS Quarterly Census of

Employment and Wages (QCEW) Data.

Boeing is the largest business in Washington's aerospace industry

Boeing is the largest aerospace business in Washington, and the state's largest private

employer. Boeing reported Washington employment at the end of 2018 was 69,800,

representing 46% of total company employment, more than in any other state. Boeing

estimates its supply chain network includes 1,500 supplier and vendor businesses in

Washington, on which the company reported spending more than $5 billion in 2017.

Exhibit 2.3: Washington has the nation’s largest share of aerospace and Boeing jobs

Source: Bureau of Labor Statistics and Boeing.

The company's aircraft deliveries have increased since 2013, and Boeing reported

delivering a record number of aircraft in 2018. Most of the aircraft were assembled in WashingtonBoeing

assembles all 737, 747, 767, 777, and Boeing Business Jets in Washington. It uses

two assembly lines for the 787 – one in Everett, Washington, and one in North

Charleston, South Carolina.. Still, airplane orders outpaced

deliveries, and Boeing states that its order backlog is more than 5,800 aircraft. The

company estimates that this backlog represents seven years of airplane production.

Exhibit 2.4: Boeing airplane deliveries have increased

Source: JLARC representation of Boeing data.

Industry has met statutory contingencies to locate a manufacturing program in

Washington

The 2013 Legislature put two contingencies in the law:

Contingency

Outcome

The preference would not take effect until a significant commercial airplane

manufacturing program was located in Washington.

The Department of Revenue (DOR) determined that the contingency was satisfied

in 2014 after Boeing located the final assembly of the 777X and its composite

wing facility in Everett.

The preferential B&O tax rate ends for the products made at the

manufacturing site if DOR determines that any portion of that program has moved

outside Washington.

This contingency has not occurred.

Influence of preferences on continued presence of industry unclear

JLARC staff are unable to determine the degree to which the aerospace tax

preferences, particularly their 2013 extension and expansion, contributed to the

continued presence of the aerospace industry in Washington.

To assess the impact of the preferences on employment and presence in the state, it

is necessary to know the extent to which businesses make decisions as a result of the

incentive. Boeing's decision to locate final assembly of the 777X and its composite

wing facility in Washington ensured that the 2013 extension of tax preferences took

effect. However, it is unknown whether the company would have made this location

decision even if the preferences had not been extended.

Research literature and staff interviews with subject matter experts indicate that

taxes – and the availability of tax incentives – are just one of many factors that

influence business location decisions. Other factors include the quality of

transportation infrastructure, labor costs, workforce quality, and the regulatory

environment.

While some literature indicates that tax preferences influence a minority of

business location decisions, using such a general assumption is not possible when

evaluating an incentive's impact on a single location decision.

An advisory panel of economic and labor experts convened by JLARC staff agreed

with the staff conclusion that it is not feasible to analytically determine whether

one factor (e.g., tax incentives) led a single business to make a location decision.

For additional analysis of Boeing's potential location decisions, refer to Tab

4.

Preliminary Report | Aerospace Tax Preferences

Updated August 21, 2019

Review Details

3. Jobs above 2003 level, but decline since 2013 highest in the nation

Washington's aerospace employment is higher than when the

preferences were first enacted in 2003. However, since 2013, Washington has lost more

aerospace jobs than any other state.

Aerospace industry employment trending down, but still above 2003

Since 2003, when the preferences were first enacted, aerospace industry employment

followed two major trends:

Statewide aerospace employment (yellow line) grew from 2003 through 2012.

From 2003 through 2012, Washington aerospace employment increased by 56%, as the

state added 34,500 jobs. Of these new jobs, 32,400 were at Boeing, which increased its

employment by 60% (blue line).

Employment declined from 2012 through 2018. From 2012 through 2018, Boeing

employment in Washington fell by 16,700. This was partially offset by gains by other

aerospace businesses, so Washington's total aerospace employment fell by 10,800.

Despite the decline, statewide aerospace and Boeing employment remained 38% and 29%

above 2003 levels, respectively. JLARC staff do not assert a causal relationship between

these trends and legislative action to create the preferences in 2003 and extend them in

2013.

Exhibit 3.1: Both Boeing and statewide aerospace employment trending down since 2013,

but still above 2003 levels

Source: Bureau of Labor Statistics and Boeing.

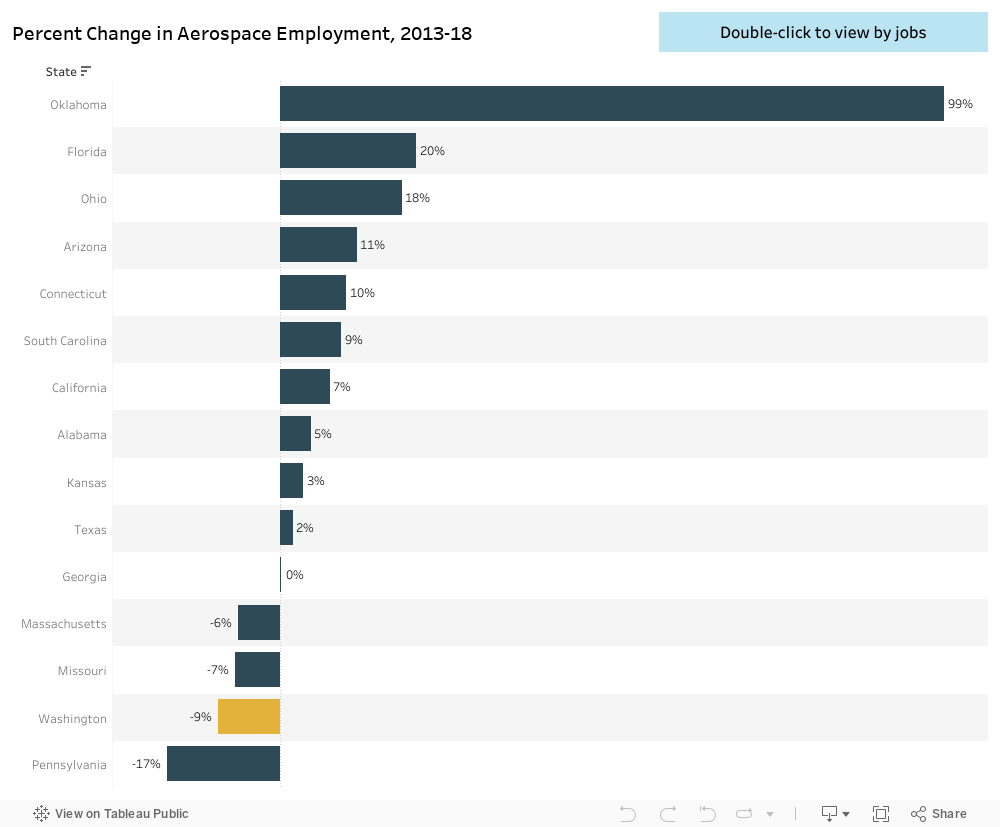

Washington aerospace employment losses since 2013 lead the nation

In 2013 the Legislature extended the aerospace tax preferences with the stated public

policy objective to maintain and grow industry employment.

Washington's loss of 8,800 aerospace jobs from 2013 through 2018 was the largest in the

U.S. and nearly four times more than in any other state. This represented a 9% decline,

the second largest percentage decline among states with at least 10,000 aerospace

employees in any year between 2013 and 2018.

Over the same period, U.S. aerospace employment (excluding Washington) increased 7%

or 27,000 jobs. This cut the state's share of total industry employment from 19% to

17%.

International aerospace employment increased 6% from 2013-17, according to data from

Deloitte.

Exhibit 3.2: Washington's aerospace employment decline was the largest among states

with a significant aerospace presence

The composition of Washington's aerospace employment has shifted, as non-Boeing

employment grew

From 2013 through 2018, Boeing employment fell by 12,100 jobs. During this period,

non-Boeing aerospace employment increased by 3,300 jobs. Boeing's share of Washington

aerospace employment fell from 87% in 2013 to 81% in 2018.

Boeing job losses were greater in Washington than in other states.

Boeing's global employment fell by 15,400 from 2013 through 2018, a 9% decline. This

decline disproportionately affected Washington, which accounted for 79% of job losses.

As a result, the state's share of Boeing employment declined from 49% to 46%.

Boeing's Washington employment rebounded from 2017 to 2018, rising 6% to 69,800. Total

company employment also grew in this period, resulting in a 1-percentage-point reduction

in Washington's share of company employment.

Non-tax factors contribute to employment changes, but the extent of their effect is

unclear

Media coverage of Boeing's wing facility has drawn increased attention to the role of

technology and automation in aerospace manufacturing. From 2003 through 2018,

Washington's aerospace industry saw increases in both output per employee (i.e., labor

productivity) and total employment. OutputMeasured as gross business income per employee

increased 83% from $565,000 in 2003 to $1,032,000 in 2018, while employment was up 38%.

However, the effect of labor productivity growth on employment is unclear. Some

literature points to outsourcing, rather than automation, as a driver of manufacturing

employment changes. JLARC staff are unable to quantify the extent to which productivity

changes influenced aerospace employment independent of other factors.

It is unclear whether industry employment meets legislative expectations

Without further information about the Legislature's expectations for aerospace industry

employment, JLARC staff are unable to determine whether recent changes meet the public

policy objective to maintain and grow aerospace industry jobs.

Preliminary Report | Aerospace Tax Preferences

Updated August 21, 2019

Review Details

4. Effect of preferences on jobs unclear

If the preferences led Boeing to remain in Washington, they may

have kept the state from losing more jobs. If not, they reduced government spending and

may have contributed to job losses.

How did extending the preferences affect employment? It depends on whether they

influenced Boeing's decision to remain in Washington.

In extending the aerospace tax preferences, the Legislature sought to secure final

assembly of the new 777X and the composite wing facility in Washington. As required,

Boeing located its new facility in Washington. It is unclear whether Boeing would have

made the same decision if the preferences had not been extended. Whether Boeing was

influenced by the preferences has direct implications on the effect of the extension

on employment.

JLARC staff modeled three hypothetical scenarios of what could have happened if the

preferences were not extended. They illustrate a range of potential employment

outcomes.

Reading the results of the economic analysis

Model results are presented as jobs potentially lost or gained as a result of

Boeing's decisions in the event the preferences had not been extended.

Total jobs includes jobs in three categories: "State and Local

Government," "Aerospace Products and Parts Manufacturing," and "Private

Nonfarm (Excluding Aerospace)."

The job numbers include direct, indirect, and induced jobs. See

Appendix C for explanations of these terms.

JLARC staff used REMIThe Regional

Economic Models, Inc. (REMI) model can be used to estimate the effects of a policy

change to model three hypothetical scenarios that illustrate the

range of what could have happened if the Legislature had not extended the preferences

in 2013. JLARC staff developed assumptions based on discussions with an advisory

group, testimony in support of the 2013 legislation extending the preferences, and

estimates of Boeing's direct 777 workforce. Because REMI is calibrated to Washington's

economy in 2016, the first year of the analysis is 2017.

JLARC staff are not able to determine the likelihood that any of these scenarios

would have occurred absent the extension of the tax preferences, or whether one is

more likely to have occurred than another. They serve to illustrate the range of

potential outcomes and the large employment multiplier of aerospace jobs in

Washington's economy.

Appendix D provides additional detail about the REMI analysis.

If the preferences led to Boeing's location decision, they may have prevented

greater job losses

Aerospace employment has decreased since 2013 when the preferences were extended (Tab

3). However, scenarios 1 and 2 model the removal of additional aerospace jobs to

simulate Boeing's decision to move airplane production out of state. The decline in

aerospace jobs leads to a much larger drop in private sector employment, due to the

high multiplier effect of aerospace jobs.

In the REMI model, aerospace jobs have a multiplier of over 4, meaning that for

every aerospace job lost, an additional four jobs are lost economy-wide.

The high multiplier stems from the industry's high wages (e.g., supporting jobs in

retail or construction) and from the number of industries in Washington that supply

goods and services to the aerospace industry (e.g., engineering services and machine

shops).

Scenario 1: Boeing locates 777X production and the composite wing facility outside

Washington. Boeing's decision to move the 777X out of state has no bearing on location

decisions for future aircraft lines.

Assumptions

The preferences were not extended, and as a result:

Boeing moves 12,100 employeesEstimated 777X workforce out of state over five years as

777X production ramps up and production of the old model is phased out.

Boeing builds the composite wing facility outside Washington, and the

state forgoes the benefits of $1 billion in construction and 500 jobs at the

wing facility.

State government spending increases beginning in 2025 due to higher tax

revenue as the preferences expire. Beneficiary production costs are

increased by the same amount.

Results

The hypothetical loss of the 777X production line results in the loss of

70,400 jobs statewide by 2021 (estimated).

Employment rebounds slightly when

the original preferences expire in 2025, resulting in an increase in revenue

collection and government spending.

By 2040, REMI estimates total job losses of 71,600.

Exhibit 4.1: Scenario 1 shows a hypothetical loss of 12,100 Boeing jobs linked to

777X production could have resulted in loss of an estimated 71,600 jobs statewide

Source: JLARC staff analysis using REMI.

Scenario 2: Boeing locates 777X production and subsequent generations of airplanes

outside Washington.

Assumptions

The preferences were not extended, and as a result:

Boeing moves 80%This

scenario was considered by the Office of Financial Management (OFM) in

its analysis for the 2003 aerospace tax preferences and was included in

JLARC's 2014 report on the preferences. of its workforce

(estimated at 60,500 employees) out of state over fifteen years, as all new

production lines are sited out of Washington.

Boeing builds the composite wing facility outside Washington, and the

state forgoes the benefits of $1 billion in construction and 500 jobs at the

wing facility.

State government spending is increased beginning in 2025 due to higher tax

revenue as the preferences expire. Beneficiary production costs are

increased by the same amount.

Results

The hypothetical loss of Boeing jobs results in the loss of 340,600 jobs

statewide by 2031 (estimated).

Total job losses reach an estimated 364,500

by 2040.

Exhibit 4.2: Scenario 2 shows a hypothetical loss of 80% of Boeing jobs for new

production lines could have resulted in loss of an estimated 364,500 jobs statewide

Source: JLARC staff analysis using REMI.

If the location decision happened regardless of the preferences, then they reduced

overall statewide employment after 2025

Scenario 3, models the effect if Boeing built the 777X and composite wing facility in

Washington without the tax preferences. The implicit assumption is that the

preferences – if passed – would have had no effect on the company's decision.

Scenario 3: Boeing sites 777X production in Washington despite the preferences not

being expanded and extended.

Assumptions

The preferences were not extended. Boeing builds the 777X in Everett without

them, and as a result:

Government spending is increased beginning in 2025, as the expiration of

the preferences leads to higher tax receipts.

Beneficiary production costs are increased by the same amount as the

additional tax revenue.

Employment and capital expenditures are unchanged from the baseline.

However, the capital expenditure is subject to sales and use tax, as this

expenditure would not have qualified for the exemption absent the 2013

expansion.

Results

The impacts to employment result from the non-expansion and subsequent

expiration of the preferences:

Absent the expansion of the sales and use tax exemption for airplane

manufacturing facilities, the tax due on the composite wing facility's

construction is estimated to contribute to a small employment decline in the

early years of the forecast.

Higher production costs due to the expiration of tax savings result in a

drop in aerospace employment beginning in 2025, with the decrease reaching

200 by 2040.

Statewide employment is largely unchanged from the baseline until 2025,

when the preferences' expiration increases government spending by an amount

equal to estimated beneficiary savings.

All of these effects net to an estimated 4,700 job increase by 2040.

Exhibit 4.3: Scenario 3 indicates if 777X siting would have happened without tax

preferences, increase in government spending could have offset minor aerospace job

losses

Source: JLARC staff analysis using REMI.

The Legislative Auditor cannot determine if the preferences maintained or grew

aerospace employment

Since there is uncertainty as to how the preferences influenced Boeing's facility

location decision, it is not possible to draw a definitive conclusion about whether

the preferences resulted in maintaining or growing employment.

Preliminary Report | Aerospace Tax Preferences

Updated August 21, 2019

Review Details

Section 5: Applicable Statutes

The aerospace tax preferences are codified in several sections of

statute

If only selected language in a section of law is relevant, that relevant language is

highlighted.

(1) Upon every person engaging within this state in the business of making sales at

retail, except persons taxable as retailers under other provisions of this chapter, as

to such persons, the amount of tax with respect to such business is equal to the gross

proceeds of sales of the business, multiplied by the rate of 0.471 percent.

(2) Upon every person engaging within this state in the business of making sales at

retail that are exempt from the tax imposed under chapter 82.08 RCW by reason of RCW

82.08.0261, 82.08.0262, or 82.08.0263, except persons taxable under RCW 82.04.260(11)

or subsection (3) of this section, as to such persons, the amount of tax with respect

to such business is equal to the gross proceeds of sales of the business, multiplied

by the rate of 0.484 percent.

(3)(a) Until July 1, 2040, upon every person

classified by the federal aviation administration as a federal aviation regulation

part 145 certificated repair station and that is engaging within this state in the

business of making sales at retail that are exempt from the tax imposed under

chapter 82.08 RCW by reason of RCW 82.08.0261, 82.08.0262, or 82.08.0263, as to such

persons, the amount of tax with respect to such business is equal to the gross

proceeds of sales of the business, multiplied by the rate of .2904

percent.

(b) A person reporting under the tax rate

provided in this subsection (3) must file a complete annual report with the

department under RCW 82.32.534.

[ 2014 c 97 § 402; (2014 c 97 § 401 expired July 9, 2014); 2013 3rd sp.s. c 2 § 7;

2010 1st sp.s. c 23 § 509; (2010 1st sp.s. c 23 § 508 expired July 1, 2011); (2010 1st

sp.s. c 23 § 507 expired July 13, 2010); 2010 1st sp.s. c 11 § 1; (2010 c 114 § 106

expired July 1, 2011); 2008 c 81 § 5; (2007 c 54 § 5 repealed by 2010 1st sp.s. c 11 §

7); 2006 c 177 § 5; 2003 2nd sp.s. c 1 § 2; (2003 1st sp.s. c 2 § 1 expired July 1,

2006). Prior: 1998 c 343 § 5; 1998 c 312 § 4; 1993 sp.s. c 25 § 103; 1981 c 172 § 2;

1971 ex.s. c 281 § 4; 1971 ex.s. c 186 § 2; 1969 ex.s. c 262 § 35; 1967 ex.s. c 149 §

9; 1961 c 15 § 82.04.250; prior: 1955 c 389 § 45; prior: 1950 ex.s. c 5 § 1, part;

1949 c 228 § 1, part; 1943 c 156 § 1, part; 1941 c 178 § 1, part; 1939 c 225 § 1,

part; 1937 c 227 § 1, part; 1935 c 180 § 4, part; Rem. Supp. 1949 § 8370-4, part.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Findings—Savings—Effective date—2008 c 81: See notes following RCW 82.08.975.

Finding—2003 2nd sp.s. c 1: See note following RCW 82.04.4461.

Tax on manufacturers and processors of various foods and by-products—Research and

development organizations—Travel agents—Certain international activities—Stevedoring

and associated activities—Low-level waste disposers—Insurance producers, surplus line

brokers, and title insurance agents—Hospitals—Commercial airplane activities—Timber

product activities—Canned salmon processors. (Effective January 1, 2018.)

(1) Upon every person engaging within this state in the business of manufacturing:

(a) Wheat into flour, barley into pearl barley, soybeans into soybean oil, canola

into canola oil, canola meal, or canola by-products, or sunflower seeds into sunflower

oil; as to such persons the amount of tax with respect to such business is equal to

the value of the flour, pearl barley, oil, canola meal, or canola by-product

manufactured, multiplied by the rate of 0.138 percent;

(b) Beginning July 1, 2025, seafood products that remain in a raw, raw frozen, or raw

salted state at the completion of the manufacturing by that person; or selling

manufactured seafood products that remain in a raw, raw frozen, or raw salted state at

the completion of the manufacturing, to purchasers who transport in the ordinary

course of business the goods out of this state; as to such persons the amount of tax

with respect to such business is equal to the value of the products manufactured or

the gross proceeds derived from such sales, multiplied by the rate of 0.138 percent.

Sellers must keep and preserve records for the period required by RCW 82.32.070

establishing that the goods were transported by the purchaser in the ordinary course

of business out of this state;

(c)(i) Except as provided otherwise in (c)(iii) of this subsection, from July 1,

2025, until January 1, 2036, dairy products; or selling dairy products that the person

has manufactured to purchasers who either transport in the ordinary course of business

the goods out of state or purchasers who use such dairy products as an ingredient or

component in the manufacturing of a dairy product; as to such persons the tax imposed

is equal to the value of the products manufactured or the gross proceeds derived from

such sales multiplied by the rate of 0.138 percent. Sellers must keep and preserve

records for the period required by RCW 82.32.070 establishing that the goods were

transported by the purchaser in the ordinary course of business out of this state or

sold to a manufacturer for use as an ingredient or component in the manufacturing of a

dairy product. (ii) For the purposes of this subsection (1)(c), "dairy products"

means: (A) Products, not including any marijuana-infused product, that as of September

20, 2001, are identified in 21 C.F.R., chapter 1, parts 131, 133, and 135, including

by-products from the manufacturing of the dairy products, such as whey and casein; and

(B) Products comprised of not less than seventy percent dairy products that qualify

under (c)(ii)(A) of this subsection, measured by weight or volume. (iii) The

preferential tax rate provided to taxpayers under this subsection (1)(c) does not

apply to sales of dairy products on or after July 1, 2023, where a dairy product is

used by the purchaser as an ingredient or component in the manufacturing in Washington

of a dairy product;

(d)(i) Beginning July 1, 2025, fruits or vegetables by canning, preserving, freezing,

processing, or dehydrating fresh fruits or vegetables, or selling at wholesale fruits

or vegetables manufactured by the seller by canning, preserving, freezing, processing,

or dehydrating fresh fruits or vegetables and sold to purchasers who transport in the

ordinary course of business the goods out of this state; as to such persons the amount

of tax with respect to such business is equal to the value of the products

manufactured or the gross proceeds derived from such sales multiplied by the rate of

0.138 percent. Sellers must keep and preserve records for the period required by RCW

82.32.070 establishing that the goods were transported by the purchaser in the

ordinary course of business out of this state. (ii) For purposes of this subsection

(1)(d), "fruits" and "vegetables" do not include marijuana, useable marijuana, or

marijuana-infused products;

(e) Until July 1, 2009, alcohol fuel, biodiesel fuel, or biodiesel feedstock, as

those terms are defined in RCW 82.29A.135; as to such persons the amount of tax with

respect to the business is equal to the value of alcohol fuel, biodiesel fuel, or

biodiesel feedstock manufactured, multiplied by the rate of 0.138 percent; and

(f) Wood biomass fuel as defined in RCW 82.29A.135; as to such persons the amount of

tax with respect to the business is equal to the value of wood biomass fuel

manufactured, multiplied by the rate of 0.138 percent.

(2) Upon every person engaging within this state in the business of splitting or

processing dried peas; as to such persons the amount of tax with respect to such

business is equal to the value of the peas split or processed, multiplied by the rate

of 0.138 percent.

(3) Upon every nonprofit corporation and nonprofit association engaging within this

state in research and development, as to such corporations and associations, the

amount of tax with respect to such activities is equal to the gross income derived

from such activities multiplied by the rate of 0.484 percent.

(4) Upon every person engaging within this state in the business of slaughtering,

breaking and/or processing perishable meat products and/or selling the same at

wholesale only and not at retail; as to such persons the tax imposed is equal to the

gross proceeds derived from such sales multiplied by the rate of 0.138 percent.

(5) Upon every person engaging within this state in the business of acting as a

travel agent or tour operator; as to such persons the amount of the tax with respect

to such activities is equal to the gross income derived from such activities

multiplied by the rate of 0.275 percent.

(6) Upon every person engaging within this state in business as an international

steamship agent, international customs house broker, international freight forwarder,

vessel and/or cargo charter broker in foreign commerce, and/or international air cargo

agent; as to such persons the amount of the tax with respect to only international

activities is equal to the gross income derived from such activities multiplied by the

rate of 0.275 percent.

(7) Upon every person engaging within this state in the business of stevedoring and

associated activities pertinent to the movement of goods and commodities in waterborne

interstate or foreign commerce; as to such persons the amount of tax with respect to

such business is equal to the gross proceeds derived from such activities multiplied

by the rate of 0.275 percent. Persons subject to taxation under this subsection are

exempt from payment of taxes imposed by chapter 82.16 RCW for that portion of their

business subject to taxation under this subsection. Stevedoring and associated

activities pertinent to the conduct of goods and commodities in waterborne interstate

or foreign commerce are defined as all activities of a labor, service or

transportation nature whereby cargo may be loaded or unloaded to or from vessels or

barges, passing over, onto or under a wharf, pier, or similar structure; cargo may be

moved to a warehouse or similar holding or storage yard or area to await further

movement in import or export or may move to a consolidation freight station and be

stuffed, unstuffed, containerized, separated or otherwise segregated or aggregated for

delivery or loaded on any mode of transportation for delivery to its consignee.

Specific activities included in this definition are: Wharfage, handling, loading,

unloading, moving of cargo to a convenient place of delivery to the consignee or a

convenient place for further movement to export mode; documentation services in

connection with the receipt, delivery, checking, care, custody and control of cargo

required in the transfer of cargo; imported automobile handling prior to delivery to

consignee; terminal stevedoring and incidental vessel services, including but not

limited to plugging and unplugging refrigerator service to containers, trailers, and

other refrigerated cargo receptacles, and securing ship hatch covers.

(8)(a) Upon every person engaging within this state in the business of disposing of

low-level waste, as defined in RCW 43.145.010; as to such persons the amount of the

tax with respect to such business is equal to the gross income of the business,

excluding any fees imposed under chapter 43.200 RCW, multiplied by the rate of 3.3

percent.

(b) If the gross income of the taxpayer is attributable to activities both within and

without this state, the gross income attributable to this state must be determined in

accordance with the methods of apportionment required under RCW 82.04.460.

(9) Upon every person engaging within this state as an insurance producer or title

insurance agent licensed under chapter 48.17 RCW or a surplus line broker licensed

under chapter 48.15 RCW; as to such persons, the amount of the tax with respect to

such licensed activities is equal to the gross income of such business multiplied by

the rate of 0.484 percent.

(10) Upon every person engaging within this state in business as a hospital, as

defined in chapter 70.41 RCW, that is operated as a nonprofit corporation or by the

state or any of its political subdivisions, as to such persons, the amount of tax with

respect to such activities is equal to the gross income of the business multiplied by

the rate of 0.75 percent through June 30, 1995, and 1.5 percent thereafter.

(11)(a) Beginning October 1, 2005, upon every person engaging within this state in

the business of manufacturing commercial airplanes, or components of such airplanes,

or making sales, at retail or wholesale, of commercial airplanes or components of

such airplanes, manufactured by the seller, as to such persons the amount of tax

with respect to such business is, in the case of manufacturers, equal to the value

of the product manufactured and the gross proceeds of sales of the product

manufactured, or in the case of processors for hire, equal to the gross income of

the business, multiplied by the rate of: (i) 0.4235 percent from October 1, 2005,

through June 30, 2007; and (ii) 0.2904 percent beginning July 1, 2007.

(b) Beginning July 1, 2008, upon every person who is not eligible to report under

the provisions of (a) of this subsection (11) and is engaging within this state in

the business of manufacturing tooling specifically designed for use in manufacturing

commercial airplanes or components of such airplanes, or making sales, at retail or

wholesale, of such tooling manufactured by the seller, as to such persons the amount

of tax with respect to such business is, in the case of manufacturers, equal to the

value of the product manufactured and the gross proceeds of sales of the product

manufactured, or in the case of processors for hire, be equal to the gross income of

the business, multiplied by the rate of 0.2904 percent.

(c) For the purposes of this subsection (11),

"commercial airplane" and "component" have the same meanings as provided in RCW

82.32.550.

(d) In addition to all other requirements

under this title, a person reporting under the tax rate provided in this subsection

(11) must file a complete annual tax performance report with the department under

RCW 82.32.534.

(e)(i) Except as provided in (e)(ii) of this

subsection (11), this subsection (11) does not apply on and after July 1, 2040. (ii)

With respect to the manufacturing of commercial airplanes or making sales, at retail

or wholesale, of commercial airplanes, this subsection (11) does not apply on and

after July 1st of the year in which the department makes a determination that any

final assembly or wing assembly of any version or variant of a commercial airplane

that is the basis of a siting of a significant commercial airplane manufacturing

program in the state under RCW 82.32.850 has been sited outside the state of

Washington. This subsection (11)(e)(ii) only applies to the manufacturing or sale of

commercial airplanes that are the basis of a siting of a significant commercial

airplane manufacturing program in the state under RCW 82.32.850.

(12)(a) Until July 1, 2024, upon every person engaging within this state in the

business of extracting timber or extracting for hire timber; as to such persons the

amount of tax with respect to the business is, in the case of extractors, equal to the

value of products, including by-products, extracted, or in the case of extractors for

hire, equal to the gross income of the business, multiplied by the rate of 0.4235

percent from July 1, 2006, through June 30, 2007, and 0.2904 percent from July 1,

2007, through June 30, 2024.

(b) Until July 1, 2024, upon every person engaging within this state in the business

of manufacturing or processing for hire: (i) Timber into timber products or wood

products; or (ii) timber products into other timber products or wood products; as to

such persons the amount of the tax with respect to the business is, in the case of

manufacturers, equal to the value of products, including by-products, manufactured, or

in the case of processors for hire, equal to the gross income of the business,

multiplied by the rate of 0.4235 percent from July 1, 2006, through June 30, 2007, and

0.2904 percent from July 1, 2007, through June 30, 2024.

(c) Until July 1, 2024, upon every person engaging within this state in the business

of selling at wholesale: (i) Timber extracted by that person; (ii) timber products

manufactured by that person from timber or other timber products; or (iii) wood

products manufactured by that person from timber or timber products; as to such

persons the amount of the tax with respect to the business is equal to the gross

proceeds of sales of the timber, timber products, or wood products multiplied by the

rate of 0.4235 percent from July 1, 2006, through June 30, 2007, and 0.2904 percent

from July 1, 2007, through June 30, 2024.

(d) Until July 1, 2024, upon every person engaging within this state in the business

of selling standing timber; as to such persons the amount of the tax with respect to

the business is equal to the gross income of the business multiplied by the rate of

0.2904 percent. For purposes of this subsection (12)(d), "selling standing timber"

means the sale of timber apart from the land, where the buyer is required to sever the

timber within thirty months from the date of the original contract, regardless of the

method of payment for the timber and whether title to the timber transfers before,

upon, or after severance.

(e) For purposes of this subsection, the following definitions apply: (i)

"Biocomposite surface products" means surface material products containing, by weight

or volume, more than fifty percent recycled paper and that also use nonpetroleum-based

phenolic resin as a bonding agent. (ii) "Paper and paper products" means products made

of interwoven cellulosic fibers held together largely by hydrogen bonding. "Paper and

paper products" includes newsprint; office, printing, fine, and pressure-sensitive

papers; paper napkins, towels, and toilet tissue; kraft bag, construction, and other

kraft industrial papers; paperboard, liquid packaging containers, containerboard,

corrugated, and solid-fiber containers including linerboard and corrugated medium; and

related types of cellulosic products containing primarily, by weight or volume,

cellulosic materials. "Paper and paper products" does not include books, newspapers,

magazines, periodicals, and other printed publications, advertising materials,

calendars, and similar types of printed materials. (iii) "Recycled paper" means paper

and paper products having fifty percent or more of their fiber content that comes from

postconsumer waste. For purposes of this subsection (12)(e)(iii), "postconsumer waste"

means a finished material that would normally be disposed of as solid waste, having

completed its life cycle as a consumer item. (iv) "Timber" means forest trees,

standing or down, on privately or publicly owned land. "Timber" does not include

Christmas trees that are cultivated by agricultural methods or short-rotation

hardwoods as defined in RCW 84.33.035. (v) "Timber products" means: (A) Logs, wood

chips, sawdust, wood waste, and similar products obtained wholly from the processing

of timber, short-rotation hardwoods as defined in RCW 84.33.035, or both; (B) Pulp,

including market pulp and pulp derived from recovered paper or paper products; and (C)

Recycled paper, but only when used in the manufacture of biocomposite surface

products. (vi) "Wood products" means paper and paper products; dimensional lumber;

engineered wood products such as particleboard, oriented strand board, medium density

fiberboard, and plywood; wood doors; wood windows; and biocomposite surface products.

(f) Except for small harvesters as defined in RCW 84.33.035, a person reporting under

the tax rate provided in this subsection (12) must file a complete annual tax

performance report with the department under RCW 82.32.534.

(13) Upon every person engaging within this state in inspecting, testing, labeling,

and storing canned salmon owned by another person, as to such persons, the amount of

tax with respect to such activities is equal to the gross income derived from such

activities multiplied by the rate of 0.484 percent.

(14)(a) Upon every person engaging within this state in the business of printing a

newspaper, publishing a newspaper, or both, the amount of tax on such business is

equal to the gross income of the business multiplied by the rate of 0.35 percent until

July 1, 2024, and 0.484 percent thereafter.

(b) A person reporting under the tax rate provided in this subsection (14) must file

a complete annual tax performance report with the department under RCW 82.32.534.

[ 2018 c 164 § 3; 2017 c 135 § 11. Prior: 2015 3rd sp.s. c 6 § 602; 2015 3rd sp.s. c

6 § 205; prior: 2014 c 140 § 6; (2014 c 140 § 5 expired July 1, 2015); 2014 c 140 § 4;

(2014 c 140 § 3 expired July 1, 2015); 2013 3rd sp.s. c 2 § 6; (2013 3rd sp.s. c 2 § 5

expired July 1, 2015); 2013 2nd sp.s. c 13 § 203; (2013 2nd sp.s. c 13 § 202 expired

July 1, 2015); prior: (2012 2nd sp.s. c 6 § 602 expired July 1, 2015); 2012 2nd sp.s.

c 6 § 204; 2011 c 2 § 203 (Initiative Measure No. 1107, approved November 2, 2010);

2010 1st sp.s. c 23 § 506; (2010 1st sp.s. c 23 § 505 expired June 10, 2010); 2010 c

114 § 107; prior: 2009 c 479 § 64; 2009 c 461 § 1; 2009 c 162 § 34; prior: 2008 c 296

§ 1; 2008 c 217 § 100; 2008 c 81 § 4; prior: 2007 c 54 § 6; 2007 c 48 § 2; prior: 2006

c 354 § 4; 2006 c 300 § 1; prior: 2005 c 513 § 2; 2005 c 443 § 4; prior: 2003 2nd

sp.s. c 1 § 4; 2003 2nd sp.s. c 1 § 3; 2003 c 339 § 11; 2003 c 261 § 11; 2001 2nd

sp.s. c 25 § 2; prior: 1998 c 312 § 5; 1998 c 311 § 2; prior: 1998 c 170 § 4; 1996 c

148 § 2; 1996 c 115 § 1; prior: 1995 2nd sp.s. c 12 § 1; 1995 2nd sp.s. c 6 § 1; 1993

sp.s. c 25 § 104; 1993 c 492 § 304; 1991 c 272 § 15; 1990 c 21 § 2; 1987 c 139 § 1;

prior: 1985 c 471 § 1; 1985 c 135 § 2; 1983 2nd ex.s. c 3 § 5; prior: 1983 1st ex.s. c

66 § 4; 1983 1st ex.s. c 55 § 4; 1982 2nd ex.s. c 13 § 1; 1982 c 10 § 16; prior: 1981

c 178 § 1; 1981 c 172 § 3; 1979 ex.s. c 196 § 2; 1975 1st ex.s. c 291 § 7; 1971 ex.s.

c 281 § 5; 1971 ex.s. c 186 § 3; 1969 ex.s. c 262 § 36; 1967 ex.s. c 149 § 10; 1965

ex.s. c 173 § 6; 1961 c 15 § 82.04.260; prior: 1959 c 211 § 2; 1955 c 389 § 46; prior:

1953 c 91 § 4; 1951 2nd ex.s. c 28 § 4; 1950 ex.s. c 5 § 1, part; 1949 c 228 § 1,

part; 1943 c 156 § 1, part; 1941 c 178 § 1, part; 1939 c 225 § 1, part; 1937 c 227 §

1, part; 1935 c 180 § 4, part; Rem. Supp. 1949 § 8370-4, part.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Findings—Savings—Effective date—2008 c 81: See notes following RCW 82.08.975.

Finding—2003 2nd sp.s. c 1: See note following RCW 82.04.4461.

Aerospace Product Development - Preferential Rate (B&O Tax)

RCW 82.04.290

Tax on international investment management services or other business or service

activities.

(1) Upon every person engaging within this state in the business of providing

international investment management services, as to such persons, the amount of tax

with respect to such business is equal to the gross income or gross proceeds of sales

of the business multiplied by a rate of 0.275 percent.

(2)(a) Upon every person engaging within this state in any business activity other

than or in addition to an activity taxed explicitly under another section in this

chapter or subsection (1) or (3) of this section; as to such persons the amount of tax

on account of such activities is equal to the gross income of the business multiplied

by the rate of 1.5 percent.

(b) This subsection (2) includes, among others, and without limiting the scope hereof

(whether or not title to materials used in the performance of such business passes to

another by accession, confusion or other than by outright sale), persons engaged in

the business of rendering any type of service which does not constitute a "sale at

retail" or a "sale at wholesale." The value of advertising, demonstration, and

promotional supplies and materials furnished to an agent by his or her principal or

supplier to be used for informational, educational, and promotional purposes is not

considered a part of the agent's remuneration or commission and is not subject to

taxation under this section.

(3)(a) Until July 1, 2040, upon every person engaging within this state in the

business of performing aerospace product development for others, as to such persons,

the amount of tax with respect to such business is equal to the gross income of the

business multiplied by a rate of 0.9 percent.

(b) A person reporting under the tax rate

provided in this subsection (3) must file a complete annual report with the

department under RCW 82.32.534.

(c) "Aerospace product development" has the

meaning as provided in RCW 82.04.4461.

[ 2014 c 97 § 404; (2014 c 97 § 403 expired July 9, 2014); 2013 3rd sp.s. c 2 § 8;

2013 c 23 § 314; 2011 c 174 § 101; 2008 c 81 § 6; 2005 c 369 § 8; 2004 c 174 § 2; 2003

c 343 § 2; 2001 1st sp.s. c 9 § 6; (2001 1st sp.s. c 9 § 4 expired July 1, 2001).

Prior: 1998 c 343 § 4; 1998 c 331 § 2; 1998 c 312 § 8; 1998 c 308 § 5; 1998 c 308 § 4;

1997 c 7 § 2; 1996 c 1 § 2; 1995 c 229 § 3; 1993 sp.s. c 25 § 203; 1985 c 32 § 3; 1983

2nd ex.s. c 3 § 2; 1983 c 9 § 2; 1983 c 3 § 212; 1971 ex.s. c 281 § 8; 1970 ex.s. c 65

§ 4; 1969 ex.s. c 262 § 39; 1967 ex.s. c 149 § 14; 1963 ex.s. c 28 § 2; 1961 c 15 §

82.04.290; prior: 1959 ex.s. c 5 § 5; 1955 c 389 § 49; prior: 1953 c 195 § 2; 1950

ex.s. c 5 § 1, part; 1949 c 228 § 1, part; 1943 c 156 § 1, part; 1941 c 178 § 1, part;

1939 c 225 § 1, part; 1937 c 227 § 1, part; 1935 c 180 § 4, part; Rem. Supp. 1949 §

8370-4, part.]

SELECTED NOTES:

Contingent expiration date—2014 c 97 §§ 401 and 403: See note following RCW 82.04.250.

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Findings—Savings—Effective date—2008 c 81: See notes following RCW 82.08.975.

Aerospace Product Development Expenditures - Credit (B&O Tax)

RCW 82.04.4461

Credit—Preproduction development expenditures. (Effective January 1, 2018, until

July 1, 2040.)

(1)(a)(i) In computing the tax imposed under this chapter, a credit is allowed for

each person for qualified aerospace product development. For a person who is a

manufacturer or processor for hire of commercial airplanes or components of such

airplanes, credit may be earned for expenditures occurring after December 1, 2003. For

all other persons, credit may be earned only for expenditures occurring after June 30,

2008.(ii) For purposes of this subsection, "commercial airplane" and "component" have

the same meanings as provided in RCW 82.32.550.

(b) Before July 1, 2005, any credits earned under this section must be accrued and

carried forward and may not be used until July 1, 2005. These carryover credits may be

used at any time thereafter, and may be carried over until used. Refunds may not be

granted in the place of a credit.

(2) The credit is equal to the amount of qualified aerospace product development

expenditures of a person, multiplied by the rate of 1.5 percent.

(3) Except as provided in subsection (1)(b) of this section the credit must be

claimed against taxes due for the same calendar year in which the qualified aerospace

product development expenditures are incurred. Credit earned on or after July 1, 2005,

may not be carried over. The credit for each calendar year may not exceed the amount

of tax otherwise due under this chapter for the calendar year. Refunds may not be

granted in the place of a credit.

(4) Any person claiming the credit must file a form prescribed by the department that

must include the amount of the credit claimed, an estimate of the anticipated

aerospace product development expenditures during the calendar year for which the

credit is claimed, an estimate of the taxable amount during the calendar year for

which the credit is claimed, and such additional information as the department may

prescribe.

(5) The definitions in this subsection apply throughout this section.(a) "Aerospace

product" has the meaning given in RCW 82.08.975.(b) "Aerospace product development"

means research, design, and engineering activities performed in relation to the

development of an aerospace product or of a product line, model, or model derivative

of an aerospace product, including prototype development, testing, and certification.

The term includes the discovery of technological information, the translating of

technological information into new or improved products, processes, techniques,

formulas, or inventions, and the adaptation of existing products and models into new

products or new models, or derivatives of products or models. The term does not

include manufacturing activities or other production-oriented activities, however the

term does include tool design and engineering design for the manufacturing process.

The term does not include surveys and studies, social science and humanities research,

market research or testing, quality control, sale promotion and service, computer

software developed for internal use, and research in areas such as improved style,

taste, and seasonal design.(c) "Qualified aerospace product development" means

aerospace product development performed within this state.(d) "Qualified aerospace

product development expenditures" means operating expenses, including wages,

compensation of a proprietor or a partner in a partnership as determined by the

department, benefits, supplies, and computer expenses, directly incurred in qualified

aerospace product development by a person claiming the credit provided in this

section. The term does not include amounts paid to a person or to the state and any of

its departments and institutions, other than a public educational or research

institution to conduct qualified aerospace product development. The term does not

include capital costs and overhead, such as expenses for land, structures, or

depreciable property.(e) "Taxable amount" means the taxable amount subject to the tax

imposed in this chapter required to be reported on the person's tax returns during the

year in which the credit is claimed, less any taxable amount for which a credit is

allowed under RCW 82.04.440.

(6) In addition to all other requirements under this title, a person claiming the

credit under this section must file a complete annual tax performance report with the

department under RCW 82.32.534.

(7) Credit may not be claimed for expenditures for which a credit is claimed under

*RCW 82.04.4452.

(8) This section expires July 1, 2040.

[ 2017 c 135 § 15; 2013 3rd sp.s. c 2 § 9; 2010 c 114 § 115; 2008 c 81 § 7; 2007 c 54

§ 11; 2003 2nd sp.s. c 1 § 7.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Findings—Savings—Effective date—2008 c 81: See notes following RCW 82.08.975.

Finding—2003 2nd sp.s. c 1: "The legislature finds that the people of the

state have benefited from the presence of the aerospace industry in Washington state.

The aerospace industry provides good wages and benefits for the thousands of

engineers, mechanics, and support staff working directly in the industry throughout

the state. The suppliers and vendors that support the aerospace industry in turn

provide a range of jobs. The legislature declares that it is in the public interest to

encourage the continued presence of this industry through the provision of tax

incentives. The comprehensive tax incentives in this act address the cost of doing

business in Washington state compared to locations in other states." [ 2003 2nd sp.s.

c 1 § 1.]

Commercial Airplane Manufacturing - Credit for Taxes Paid (B&O Tax)

RCW 82.04.4463

Credit—Property and leasehold taxes paid on property used for manufacture of

commercial airplanes. (Effective January 1, 2018, until July 1, 2040.)

(1) In computing the tax imposed under this chapter, a credit is allowed for property

taxes and leasehold excise taxes paid during the calendar year.

(2) The credit is equal to:

(a)(i)(A) Property taxes paid on buildings, and land upon which the buildings are

located, constructed after December 1, 2003, and used exclusively in manufacturing

commercial airplanes or components of such airplanes; and (B) Leasehold excise taxes

paid with respect to buildings constructed after January 1, 2006, the land upon which

the buildings are located, or both, if the buildings are used exclusively in

manufacturing commercial airplanes or components of such airplanes; and(C) Property

taxes or leasehold excise taxes paid on, or with respect to, buildings constructed

after June 30, 2008, the land upon which the buildings are located, or both, and used

exclusively for aerospace product development, manufacturing tooling specifically

designed for use in manufacturing commercial airplanes or their components, or in

providing aerospace services, by persons not within the scope of (a)(i)(A) and (B) of

this subsection (2) and are taxable under RCW 82.04.290(3), 82.04.260(11)(b), or

82.04.250(3); or

(ii) Property taxes attributable to an increase in assessed value due to the

renovation or expansion, after: (A) December 1, 2003, of a building used exclusively

in manufacturing commercial airplanes or components of such airplanes; and (B) June

30, 2008, of buildings used exclusively for aerospace product development,

manufacturing tooling specifically designed for use in manufacturing commercial

airplanes or their components, or in providing aerospace services, by persons not

within the scope of (a)(ii)(A) of this subsection (2) and are taxable under RCW

82.04.290(3), 82.04.260(11)(b), or 82.04.250(3); and

(b) An amount equal to:

(i)(A) Property taxes paid, by persons taxable under RCW 82.04.260(11)(a), on

machinery and equipment exempt under RCW 82.08.02565 or 82.12.02565 and acquired after

December 1, 2003; (B) Property taxes paid, by persons taxable under RCW

82.04.260(11)(b), on machinery and equipment exempt under RCW 82.08.02565 or

82.12.02565 and acquired after June 30, 2008; or (C) Property taxes paid, by persons

taxable under RCW 82.04.250(3) or 82.04.290(3), on computer hardware, computer

peripherals, and software exempt under RCW 82.08.975 or 82.12.975 and acquired after

June 30, 2008.

(ii) For purposes of determining the amount eligible for credit under (i)(A) and (B)

of this subsection (2)(b), the amount of property taxes paid is multiplied by a

fraction. (A) The numerator of the fraction is the total taxable amount subject to the

tax imposed under RCW 82.04.260(11) (a) or (b) on the applicable business activities

of manufacturing commercial airplanes, components of such airplanes, or tooling

specifically designed for use in the manufacturing of commercial airplanes or

components of such airplanes. (B) The denominator of the fraction is the total taxable

amount subject to the tax imposed under all manufacturing classifications in chapter

82.04 RCW. (C) For purposes of both the numerator and denominator of the fraction, the

total taxable amount refers to the total taxable amount required to be reported on the

person's returns for the calendar year before the calendar year in which the credit

under this section is earned. The department may provide for an alternative method for

calculating the numerator in cases where the tax rate provided in RCW 82.04.260(11)

for manufacturing was not in effect during the full calendar year before the calendar

year in which the credit under this section is earned. (D) No credit is available

under (b)(i)(A) or (B) of this subsection (2) if either the numerator or the

denominator of the fraction is zero. If the fraction is greater than or equal to

nine-tenths, then the fraction is rounded to one. (E) As used in (b)(ii)(C) of this

subsection (2), "returns" means the tax returns for which the tax imposed under this

chapter is reported to the department.

(3) The definitions in this subsection apply throughout this section, unless the

context clearly indicates otherwise.(a) "Aerospace product development" has the same

meaning as provided in RCW 82.04.4461.(b) "Aerospace services" has the same meaning

given in RCW 82.08.975.(c) "Commercial airplane" and "component" have the same

meanings as provided in RCW 82.32.550.

(4) A credit earned during one calendar year may be carried over to be credited

against taxes incurred in a subsequent calendar year, but may not be carried over a

second year. No refunds may be granted for credits under this section.

(5) In addition to all other requirements under this title, a person claiming the

credit under this section must file a complete annual tax performance report with the

department under RCW 82.32.534.

(6) This section expires July 1, 2040.

[ 2017 c 135 § 16; 2013 3rd sp.s. c 2 § 10; 2010 1st sp.s. c 23 § 515; (2010 1st

sp.s. c 23 § 514 expired June 10, 2010); 2010 c 114 § 116; 2008 c 81 § 8; 2006 c 177 §

10; 2005 c 514 § 501; 2003 2nd sp.s. c 1 § 15.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Findings—Savings—Effective date—2008 c 81: See notes following RCW 82.08.975.

Finding—2003 2nd sp.s. c 1: See note following RCW 82.04.4461

Aerospace Product Development Computer Expenditures (Sales and Use Tax)

RCW 82.08.975

Exemptions—Computer parts and software related to the manufacture of commercial

airplanes. (Expires July 1, 2040.)

(1) The tax levied by RCW 82.08.020 does not apply to sales of computer hardware,

computer peripherals, or software, not otherwise eligible for exemption under RCW

82.08.02565, used primarily in the development, design, and engineering of aerospace

products or in providing aerospace services, or to sales of or charges made for labor

and services rendered in respect to installing the computer hardware, computer

peripherals, or software.

(2) The exemption is available only when the buyer provides the seller with an

exemption certificate in a form and manner prescribed by the department. The seller

must retain a copy of the certificate for the seller's files.

(3) The definitions in this subsection apply throughout this section unless the

context requires otherwise.

(a) "Aerospace products" means:(i) Commercial airplanes and their components;(ii)

Machinery and equipment that is designed and used primarily for the maintenance,

repair, overhaul, or refurbishing of commercial airplanes or their components by

federal aviation regulation part 145 certificated repair stations; and(iii) Tooling

specifically designed for use in manufacturing commercial airplanes or their

components.

(b) "Aerospace services" means the maintenance, repair, overhaul, or refurbishing of

commercial airplanes or their components, but only when such services are performed by

a FAR part 145 certificated repair station.

(c) "Commercial airplane" and "component" have the same meanings provided in RCW

82.32.550.

(d) "Peripherals" includes keyboards, monitors, mouse devices, and other accessories

that operate outside of the computer, excluding cables, conduit, wiring, and other

similar property.

(4) This section expires July 1, 2040.

[ 2013 3rd sp.s. c 2 § 11; 2008 c 81 § 2; 2003 2nd sp.s. c 1 § 9.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Findings—2008 c 81: "The legislature finds that the aerospace industry

provides good wages and benefits for the thousands of engineers, mechanics, support

staff, and other employees working directly in the industry throughout the state. The

legislature further finds that suppliers and vendors that support the aerospace

industry in turn provide a range of well-paying jobs. In 2003, and again in 2006, the

legislature determined it was in the public interest to encourage the continued

presence of this industry through the provision of tax incentives. However, the

legislature recognizes that key elements of Washington's aerospace industry cluster

were afforded few, if any, of the aerospace tax incentives enacted in 2003 and 2006.

The comprehensive tax incentives in this act are intended to more comprehensively

address the cost of doing business in Washington state compared to locations in other

states for a larger segment of the aerospace industry cluster." [ 2008 c 81 § 1.]

Finding—2003 2nd sp.s. c 1: See note following RCW 82.04.4461.

Commercial Airplane Production Facilities (Sales and Use Tax)

RCW 82.08.980

Exemptions—Labor, services, and personal property related to the manufacture of

commercial airplanes. (Effective January 1, 2018, until July 1, 2040.)

(1) The tax levied by RCW 82.08.020 does not apply to:

(a) Charges, for labor and services rendered in respect to the constructing of new

buildings, made to (i) a manufacturer engaged in the manufacturing of commercial

airplanes or the fuselages or wings of commercial airplanes or (ii) a port district,

political subdivision, or municipal corporation, to be leased to a manufacturer

engaged in the manufacturing of commercial airplanes or the fuselages or wings of

commercial airplanes;

(b) Sales of tangible personal property that will be incorporated as an ingredient or

component of such buildings during the course of the constructing; or

(c) Charges made for labor and services rendered in respect to installing, during the

course of constructing such buildings, building fixtures not otherwise eligible for

the exemption under RCW 82.08.02565(2)(b).

(2) The exemption is available only when the buyer provides the seller with an

exemption certificate in a form and manner prescribed by the department. The seller

must retain a copy of the certificate for the seller's files.

(3) No application is necessary for the tax exemption in this section. However, in

order to qualify under this section before starting construction, the port district,

political subdivision, or municipal corporation must have entered into an agreement

with the manufacturer to build such a facility. A person claiming the exemption under

this section is subject to all the requirements of chapter 82.32 RCW. In addition, the

person must file a complete annual tax performance report with the department under

RCW 82.32.534.

(4) The exemption in this section applies to buildings or parts of buildings,

including buildings or parts of buildings used for the storage of raw materials or

finished product, that are used primarily in the manufacturing of any one or more of

the following products:

(a) Commercial airplanes;

(b) Fuselages of commercial airplanes; or

(c) Wings of commercial airplanes.

(5) For the purposes of this section, "commercial airplane" has the meaning given in

RCW 82.32.550.

(6) This section expires July 1, 2040.

[ 2017 c 135 § 25; 2013 3rd sp.s. c 2 § 3; 2010 c 114 § 126; 2003 2nd sp.s. c 1 §

11.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Finding—2003 2nd sp.s. c 1: See note following RCW 82.04.4461.

Superefficient Airplane Production Facilities (Leasehold Excise Tax)

RCW 82.29A.137

Exemptions—Certain leasehold interests related to the manufacture of superefficient

airplanes. (Effective January 1, 2018, until July 1, 2040.)

(1) All leasehold interests in port district facilities exempt from tax under RCW

82.08.980 or 82.12.980 and used by a manufacturer engaged in the manufacturing of

superefficient airplanes, as defined in RCW 82.32.550, are exempt from tax under this

chapter. A person claiming the credit under RCW 82.04.4463 is not eligible for the

exemption under this section.

(2) In addition to all other requirements under this title, a person claiming the

exemption under this section must file a complete annual tax performance report with

the department under RCW 82.32.534.

(3) This section expires July 1, 2040.

[ 2017 c 135 § 35; 2013 3rd sp.s. c 2 § 13; 2010 c 114 § 134; 2003 2nd sp.s. c 1 §

13.]

SELECTED NOTES:

Contingent effective date—2013 3rd sp.s. c 2: See RCW 82.32.850.

Findings—Intent—2013 3rd sp.s. c 2: See note following RCW 82.32.850.

Finding—2003 2nd sp.s. c 1: See note following RCW 82.04.4461.