2022 Reviews: Five of seven Legislative Auditor recommendations require action

| In 2022, the Legislative Auditor issued seven recommendations in four separate tax preference reports as part of JLARC's annual reporting cycle. The recommendations cover preferences for commute trip reduction, food processing, nonprofit hospitals and cancer clinics, and historic auto museums. |

Five recommendations require legislative action. All but two of the preferences meet their objectives.

Commute Trip Reduction Tax Credit (B&O tax and

PUT)

Commute Trip Reduction Tax Credit (B&O tax and

PUT)

|

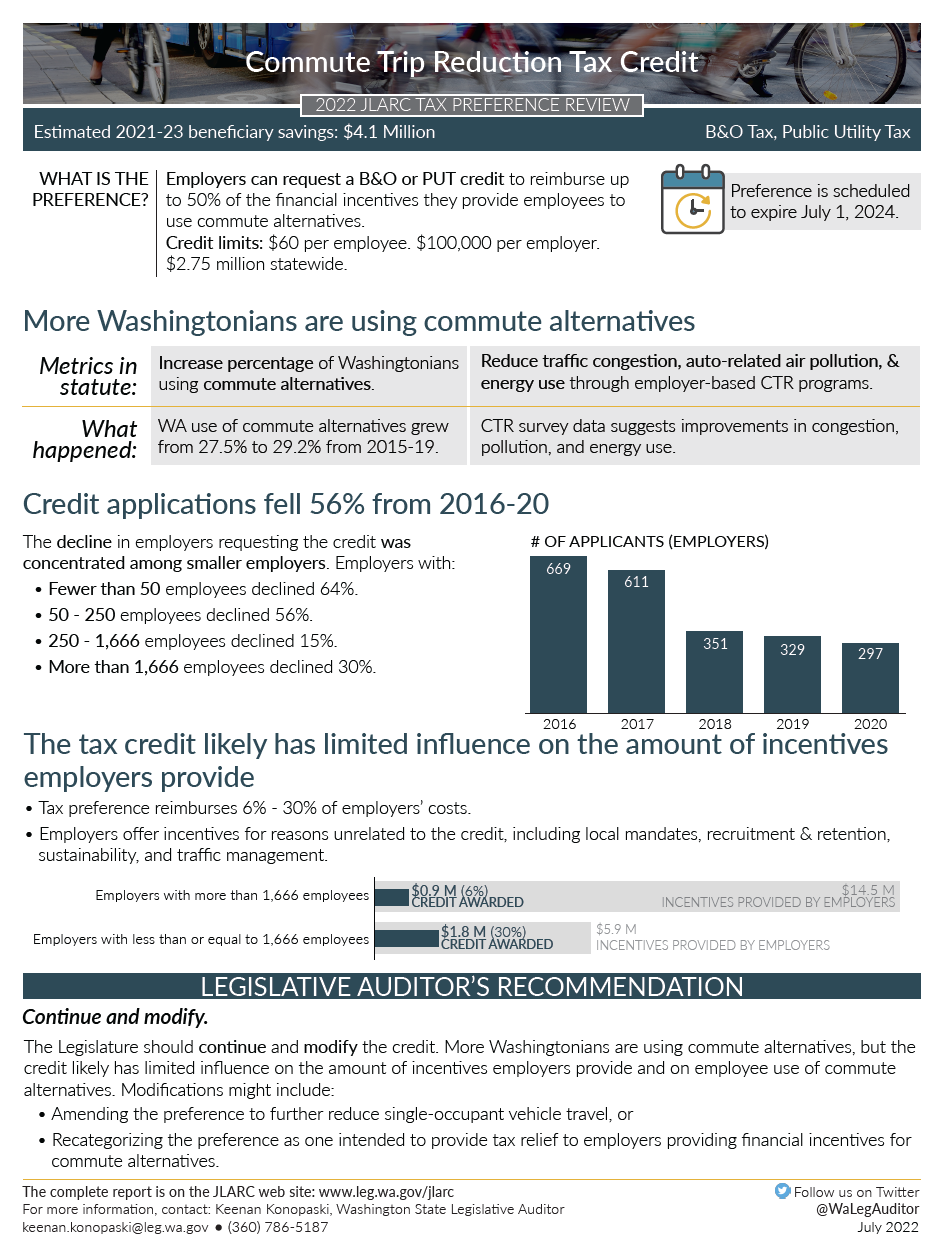

Conclusion: More Washingtonians are using commute alternatives. However, fewer employers are requesting the tax credit, and the credit likely has limited influence on the amount of financial incentives employers provide. Biennial beneficiary savings: $4.1 million Expiration date: 7/1/2024 Legislative Auditor's Recommendation: Continue and modify because the credit likely has limited influence on the amount of incentives employers provide and on employee use of commute alternatives. Commissioners' Recommendation: Available October 2022 |

Summary

|

Video Summary |

Food Processors: Dairy, Fruit and Vegetable, and Seafood Processors (B&O

tax)

|

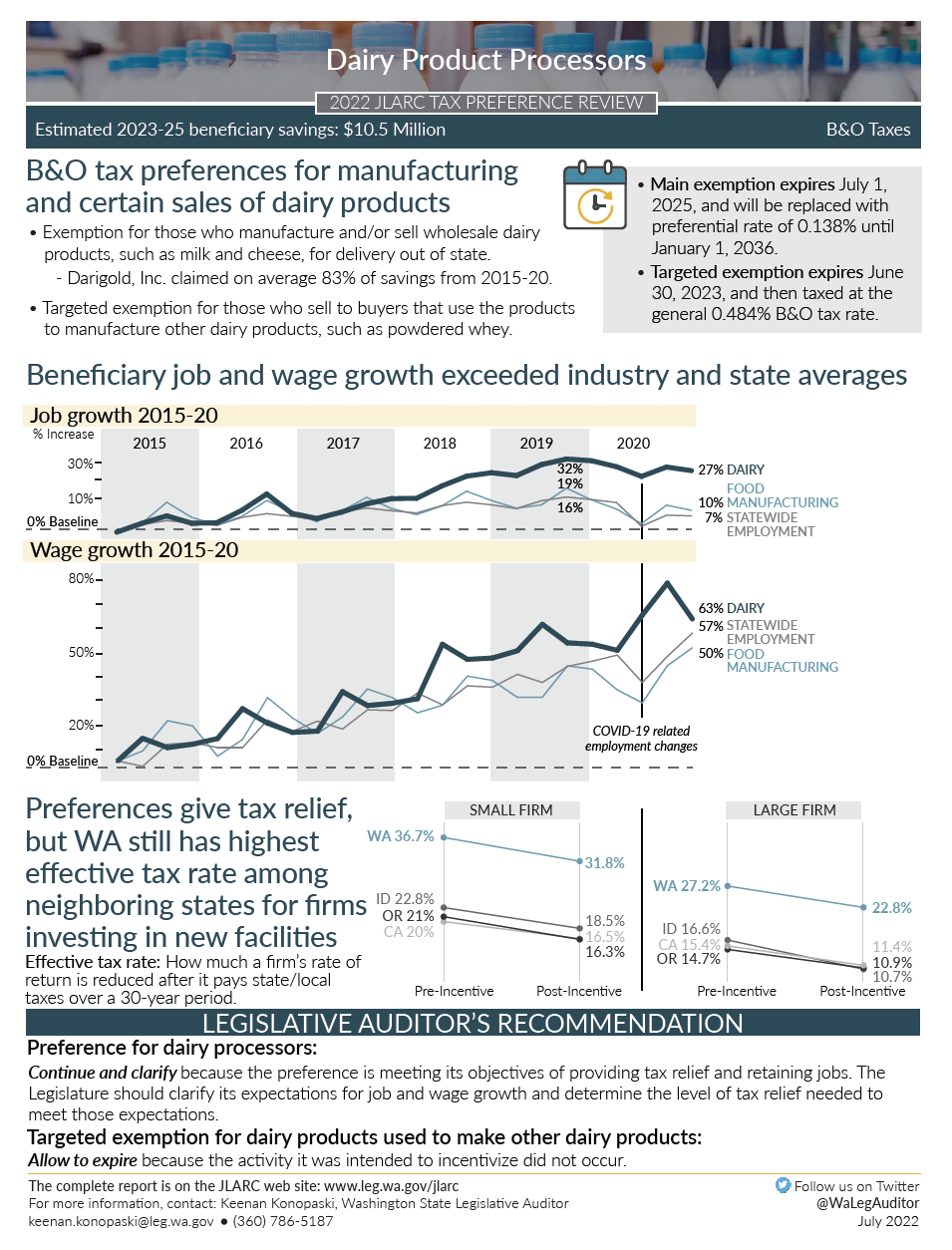

Conclusion: Dairy and fruit and vegetable beneficiaries had job and wage increases that exceeded industry and state averages. Seafood beneficiaries saw a decline in both. The preferences reduced the effective tax rates, but rates remain higher than neighboring states. Biennial beneficiary savings: Dairy: $10.5 million, Fruit & Vegetable: $22.7 million, Seafood: $4.9 million Expiration date: Exemptions expire 6/30/2025 and will be replaced with preferential rates. Legislative Auditor's Recommendation:

Commissioners' Recommendation: Available October 2022 |

Summary

|

Video Summary |

Nonprofit Hospitals and Cancer Clinics (Property tax)

|

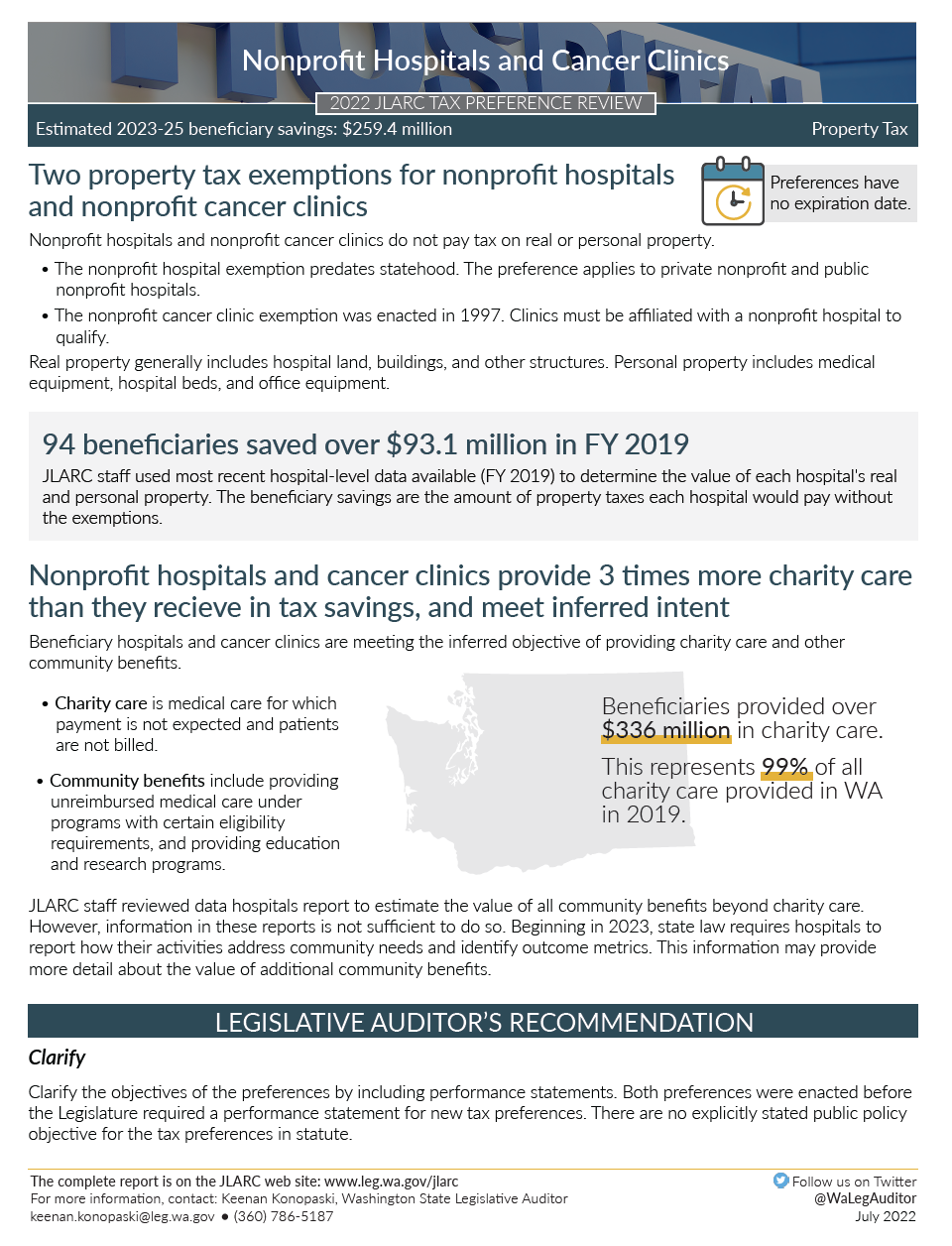

Conclusion: Property tax exemptions for nonprofit hospitals and cancer clinics meet the inferred intent of encouraging charity care and community benefits. Beneficiaries provide 99% of charity care statewide, and the value of charity care exceeds tax savings. Biennial beneficiary savings: $259.4 million Expiration date: None Legislative Auditor's Recommendation: Clarify the objectives by including performance statements. Commissioners' Recommendation: Available October 2022 |

Summary

|

Video Summary |

Two recommendations do not require legislative action

Food Processors: Dairy products used as an ingredient or component to create other

dairy products (B&O tax)

|

Conclusion: The preference was enacted in 2013 to encourage development of an infant formula production facility in Sunnyside. Industry representatives note the activity for which it was intended did not occur. Average annual savings: $62,000 Expiration date: 6/30/2023 Legislative Auditor's Recommendation: Allow to expire because the activity it was intended to incentivize did not occur. Commissioners' Recommendation: Available October 2022 |

Summary

|

Video Summary |

Historic Automobile Museums (Sales & Use tax)

|

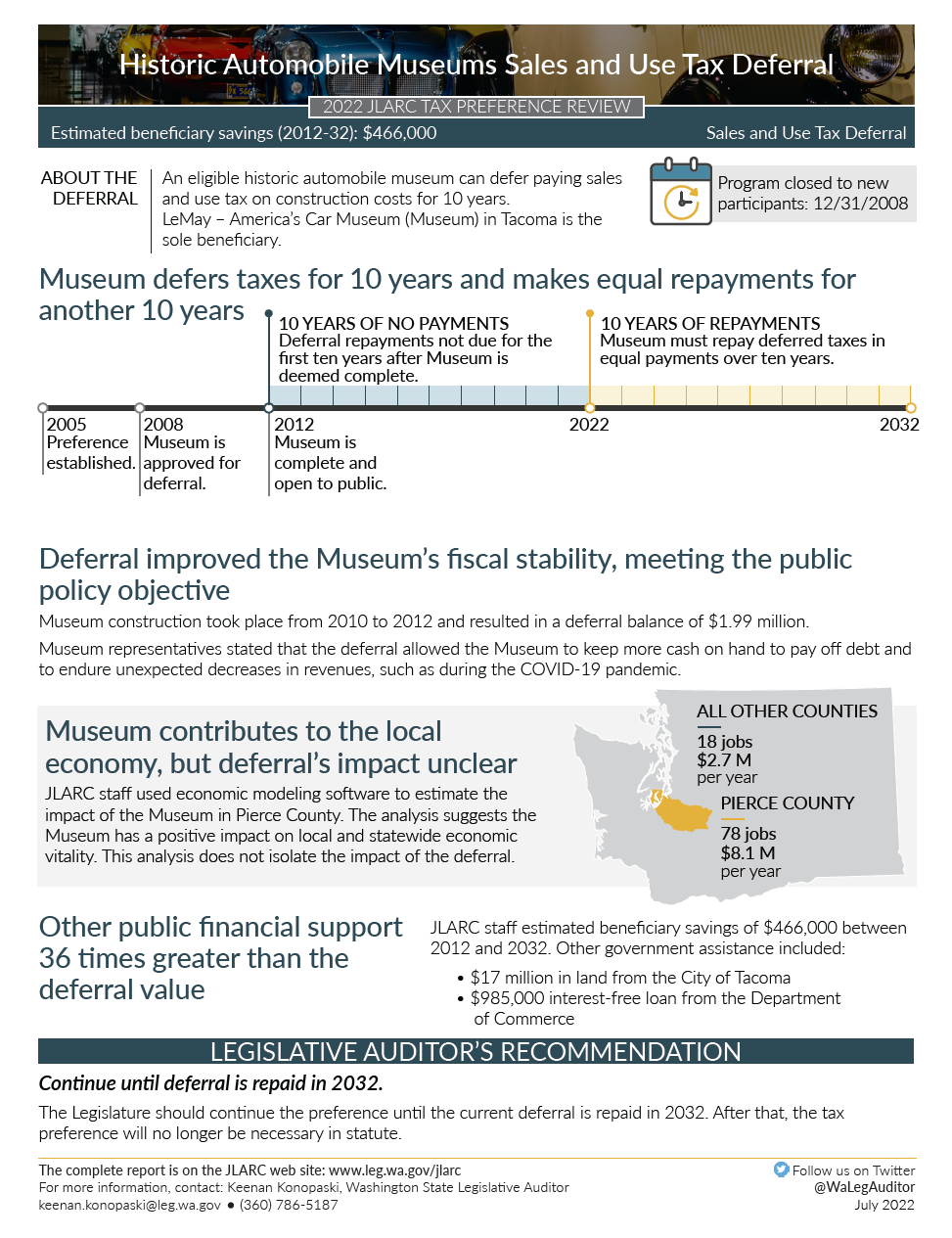

Conclusion: The tax deferral meets the public policy objective of improving the fiscal stability of its one beneficiary. This may have improved economic vitality, but other local financial incentives likely had a larger influence. Biennial beneficiary savings: $46,600 Expiration date: None Legislative Auditor's Recommendation: Continue until the deferral is repaid in 2032. Commissioners' Recommendation: Available October 2022 |

Summary

|

Video Summary |

The Citizen Commission for Performance Measurement of Tax Preferences also considers preferences based on information provided by the Department of Revenue. View the 2022 Expedited Preference Review.